UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

___________________

FORM 10-K

(MARK ONE)

|

ý

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For The Fiscal Year Ended December 31, 2011

OR

|

|

¨

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For The Transition Period from ___________ to ________

|

Commission File Number 1-33926

ARABIAN AMERICAN DEVELOPMENT COMPANY

(Exact name of registrant as specified in its charter)

|

Delaware

(State or other jurisdiction of incorporation or organization)

|

75-1256622

(I.R.S. Employer

Identification No.)

|

|

1600 Hwy 6 S, Suite 240

Sugar Land, TX

(Address of principal executive offices)

|

77478

(Zip code)

|

Registrant’s telephone number, including area code: (409) 385-8300

Securities registered pursuant to Section 12(b) of the Act:

None

Securities registered pursuant to Section 12(g) of the Act:

(Title of Class)

Common stock, par value $0.10 per share

___________________

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes¨ Noý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes¨ No ý

_____________________

Indicate by check mark whether the registrant (l) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yesý No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yesý No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company.

Large accelerated filer ¨ Accelerated filer ý

Non-accelerated filer ¨ Smaller reporting company¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act.) Yes¨ No ý

The aggregate market value on June 30, 2011, of the registrant’s voting securities held by non-affiliates was approximately $77 million.

Number of shares of registrant’s Common Stock, par value $0.10 per share, outstanding as of March 8, 2012: 23,735,165.

DOCUMENTS INCORPORATED BY REFERENCE

Part III incorporates information by reference from the definitive proxy statement for the registrant’s Annual Meeting of Stockholders to be held on or about June 6, 2012.

Item Number and Description

|

PART I

|

|

|

|

|

|

|

|

|

|

|

1 |

|

|

|

|

|

1 |

|

|

|

|

|

1 |

|

|

|

|

|

1 |

|

|

|

|

|

3 |

|

|

|

|

|

3 |

|

|

|

|

|

6 |

|

|

|

|

|

6 |

|

|

|

|

|

6 |

|

|

|

|

|

8 |

|

| |

|

|

|

|

|

|

|

|

8 |

|

| |

|

|

|

|

|

|

|

|

13 |

|

| |

|

|

|

|

|

|

|

|

13 |

|

| |

|

|

|

|

|

|

|

|

14 |

|

| |

|

|

|

|

|

|

|

|

14 |

|

| |

|

|

|

|

|

PART II

|

|

|

|

|

|

|

|

|

15 |

|

| |

|

|

|

|

|

|

|

|

16 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

16 |

|

|

|

|

|

17 |

|

|

|

|

|

17 |

|

|

|

|

|

17 |

|

|

|

|

|

21 |

|

|

|

|

|

25 |

|

|

|

|

|

27 |

|

| |

|

|

|

|

|

|

|

|

28 |

|

| |

|

|

|

|

|

|

|

|

29 |

|

| |

|

|

|

|

|

|

|

|

29 |

|

| |

|

|

|

|

|

|

|

|

29 |

|

| |

|

|

|

|

|

|

|

|

32 |

|

| |

|

|

|

|

|

PART III

|

|

|

|

|

|

|

|

|

32 |

|

| |

|

|

|

|

|

|

|

|

32 |

|

| |

|

|

|

|

|

|

|

|

32 |

|

| |

|

|

|

|

|

|

|

|

32 |

|

PART I

Arabian American Development Company (the “Company”) was incorporated in the State of Delaware in 1967. The Company’s principal business activity is the manufacturing of various specialty petrochemical products. The Company also owns a 37% interest in Al Masane Al Kobra Mining Company, a Saudi Arabian closed joint stock mining company (“AMAK”) which is just commencing commercial production of copper and zinc concentrate and a 55% interest in Pioche Ely Valley Mines, Inc. (“PEVM”), a Nevada mining corporation which presently does not conduct any substantial business activity but owns undeveloped properties in the United States. Unless the context requires otherwise, references to “we,” “us,” “our,” and the “Company” are intended to mean consolidated Arabian American Development Company and its subsidiaries. There have been no significant changes during 2011 in the method of conducting our business.

During 2011 the Company operated in one business segment; the manufacturing of various specialty petrochemical products.

Our domestic activities are primarily conducted through a wholly owned subsidiary, Texas Oil and Chemical Co. II, Inc. (the “Petrochemical Company”), which owns all of the capital stock of South Hampton Resources, Inc. (“South Hampton”). South Hampton owns and operates a specialty petrochemical facility near Silsbee, Texas which produces high purity petrochemical solvents and other petroleum based products including isopentane, normal pentane, isohexane and hexane which may be used in the production of polyethylene, packaging, polypropylene, expandable polystyrene, poly-iso/urethane foams, and in the catalyst support industry. Our petrochemical products are typically transported to customers by rail car, tank truck and iso-container. South Hampton owns all of the capital stock of Gulf State Pipe Line Company, Inc. (“Gulf State”) which owns and operates three pipelines that connect the South Hampton facility to a natural gas line, to South Hampton’s truck and rail loading terminal and to a major petroleum products pipeline owned by an unaffiliated third party.

In 2009 the Company formed South Hampton Resources International, SL (“SHRI”) located in Madrid, Spain. The Company owned 100% of the capital stock of SHRI. SHRI served as a sales office for South Hampton products in Europe and the Middle East. In May of 2011 the Spanish representative returned to the United States, and SHRI will be dissolved.

South Hampton’s specialty petrochemical facility is approximately 30 miles north of Beaumont and 90 miles east of Houston. The facility consists of seven operating units which, while interconnected, make distinct products through differing processes: (i) a Penhex Unit; (ii) a Reformer Unit; (iii) a Cyclo-pentane Unit; (iv) an Aromax® Unit; (v) an Aromatics Hydrogenation Unit; (vi) a White Oil Fractionation Unit; and (vii) a Hydrocarbon Processing Demonstration Unit. All of these units are currently in operation.

The Penhex Unit has the capacity to process approximately 6,700 barrels per day of fresh feed with the Reforming Unit, the Aromax® Unit, and the Cyclo-Pentane Unit further processing streams produced by the Penhex Unit. The Aromatics Hydrogenation Unit has a capacity of approximately 400 barrels per day, and the White Oils Fractionation Unit has a capacity of approximately 3,000 barrels per day. The Hydrocarbon Processing Demonstration Unit has a capacity of approximately 300 gallons per day. The facility generally consists of equipment commonly found in most petrochemical facilities such as fractionation towers and hydrogen treaters except the facility is adapted to produce specialized products that are high purity, very consistent, precise specification materials utilized in the petrochemical industry as solvents, additives, blowing agents and cooling agents. South Hampton produces eight distinct product streams and markets several combinations of blends as needed in various customer applications. South Hampton does not produce motor fuel products or any other commodity type products commonly sold directly to retail consumers or outlets.

Products from the Penhex Unit, Reformer Unit, Aromax® Unit, and Cyclo-pentane Unit are marketed directly to the customer by South Hampton marketing personnel. The Penhex Unit had a utilization rate during 2011 of approximately 64%. This compares to a rate of 54% for 2010. The Penhex Unit capacity was essentially doubled in 2008 and is now configured in two independent process units. The two unit configuration also improves reliability by reducing the amount of total down time due to mechanical and other factors. In October 2010 the Company completed the construction of a small Isomerization unit which provides greater flexibility in the product slate and the ability to convert a product which is less in demand, into one which is a stronger performer.

The Reformer and Aromax® Units are operated as needed to support the Penhex and Cyclo-pentane Units. Consequently, utilization rates of these units are driven by production from the Penhex Unit. Operating utilization rates are affected by product demand, mechanical integrity, and unforeseen natural occurrences, such as weather events. The nature of the petrochemical process demands periodic shut-downs for de-coking and other mechanical repairs.

The Aromatics Hydrogenation Unit, White Oils Fractionation Unit, and Hydrocarbon Processing Demonstration Unit are operated as independent and completely segregated processes. These units are dedicated to the needs of three different toll processing customers. The customers supply and maintain title to the feedstock, South Hampton processes the feedstock into products based upon customer specifications, and the customers market the products. Products may be sold directly from South Hampton’s storage tanks or transported to the customers’ location for storage and marketing. The units have a combined capacity of approximately 3,400 BPD. Together they realized a utilization rate 59% for 2011 and 53% for 2010. The units are operated in accordance with customer needs, and the contracts call for take or pay minimums of production.

South Hampton, in support of the petrochemical operation, owns approximately 75 storage tanks with total capacity approaching 225,000 barrels, and 115 acres of land at the plant site, 55 acres of which are developed. South Hampton also owns a truck and railroad loading terminal consisting of storage tanks, four rail spurs, and truck and tank car loading facilities on approximately 53 acres of which 13 acres are developed.

South Hampton obtains its feedstock requirements from a sole supplier. A contract was signed on June 1, 2004, between South Hampton and the supplier for the purchase of 65,000 barrels per month of natural gasoline on a secured basis for the period from June 1, 2004 through May 31, 2006, subsequently extended to May 31, 2007 and annually thereafter with thirty days written notice of termination by either party. In December 2006 the agreement was modified so that all purchases are simply on open account under normal credit terms and amounts owed are classified as current. The supplier built a tank to receive feedstock from a major pipeline system and provides storage for use by South Hampton. The arrangement is viewed as a means of solidifying a dependable, long term supply of feedstock for the Company. Storage fees for this arrangement were offset by the cancellation of tank rental fees in place with another party. The tank was completed in July 2007 and began full operation in October 2007.

As a result of various expansion programs and the toll processing contracts, essentially all of the standing equipment at South Hampton is operational. South Hampton has various surplus equipment stored on-site which may be used in the future to assemble additional processing units as needs arise.

Gulf State owns and operates three (3) 8-inch diameter pipelines aggregating approximately 50 miles in length connecting South Hampton’s facility to: (1) a natural gas line, (2) South Hampton’s truck and rail loading terminal and (3) a major petroleum products pipeline system owned by an unaffiliated third party. All pipelines are operated within Texas Railroad Commission and DOT regulations for maintenance and integrity.

South Hampton sells its products to predominantly Fortune 500 companies for use in the production of polyethylene, packaging, polypropylene, expandable polystyrene, poly-iso/urethane foams, and in the catalyst support industries. Products are marketed via personal contact and through continued long term relationships. Sales personnel visit customer facilities regularly and also attend various petrochemical conferences throughout the world. We have an internet presence as well. South Hampton has adopted a strategy of moving its larger volume customers to formula based pricing to reduce the effect of feedstock cost volatility. Under formula pricing the price charged to the customer is based on a formula which includes as a component the average cost of feedstock over the prior month. As a result, with this pricing mechanism, product prices move in conjunction with feedstock prices without the necessity of announced price changes. However, because the formulas use an average feedstock price from the prior month, the movement of prices will trail the movement of costs, and formula prices may or may not reflect our actual feedstock cost for the month during which the product is actually sold. In addition, while formula pricing can benefit product margins during periods of increasing feedstock costs, during periods of decreasing feedstock costs formula pricing will follow feed costs down

but will retain higher margins during the period by trailing the movement of costs by approximately 30 days. The Company believes that the use of formula pricing can reduce the volatility and increase the predictability of product margins. However, the Company continues to investigate alternative product pricing methods. During 2011 and 2010, sales to two customers exceeded 10 percent or more of the Company’s revenues. In both cases these sales represented multiple products at multiple facilities.

The Company’s only mineral interest in the United States is its 55% ownership interest in an inactive corporation, PEVM. PEVM’s properties include 48 patented and 5 unpatented claims totaling approximately 1,500 acres. All of the claims are located in Lincoln County, NV. The recent real estate devaluation nation-wide caused the Company to re-evaluate the holdings and a write down of approximately $496,000 was recorded at the end of 2008. No additional impairment was recorded in 2011, 2010, or 2009.

In late 2008 PEVM commenced dialogue with the Bureau of Land Management (“BLM”) to determine how best to remedy a potential contamination claim on neighboring property. Communication with the BLM is ongoing. PEVM has retained an environmental consultant to assist with the resolution of this matter and as of December 31, 2011, the Company had recorded a liability of $350,000 to cover estimated remediation costs as PEVM would have no other source of funds to manage the situation The Company has liens on several of the patented claims to secure the funds which have been advanced over time.

At this time, neither the Company nor PEVM have plans to develop the mining assets near Pioche, NV. Periodically proposals are received from outside parties who are interested in developing or using certain assets. Management does not anticipate making any significant domestic mining capital expenditures.

General. The Company’s operations are subject to stringent and complex federal, state, local and foreign laws and regulations relating to release of hazardous substances or wastes into the environment or otherwise relating to protection of the environment. As with the industry generally, compliance with existing and anticipated environmental laws and regulations increases our overall costs of doing business, including costs of planning, constructing, and operating plants, pipelines, and other facilities. Included in our construction and operation costs are capital cost items necessary to maintain or upgrade equipment and facilities. Similar costs are likely upon changes in laws or regulations and upon any future acquisition of operating assets.

Any failure to comply with applicable environmental laws and regulations, including those relating to equipment failures and obtaining required governmental approvals, may result in the assessment of administrative, civil or criminal penalties, imposition of investigatory or remedial activities and, in less common circumstances, issuance of injunctions or construction bans or delays. We believe that we currently hold all material governmental approvals required to operate our major facilities. As part of the regular overall evaluation of our operations, we have implemented procedures to review and update governmental approvals as necessary. We believe that our operations and facilities are in substantial compliance with applicable environmental laws and regulations and that the cost of compliance with such laws and regulations currently in effect will not have a material adverse effect on our operating results or financial condition.

The clear trend in environmental regulation is to place more restrictions and limitations on activities that may affect the environment, and thus there can be no assurance as to the amount or timing of future expenditures for environmental compliance or remediation, and actual future expenditures may be different from the amounts we currently anticipate. Moreover, risks of process upsets, accidental releases, or spills are associated with our possible future operations, and we cannot assure you that we will not incur significant costs and liabilities, including those relating to claims for damage to property and persons as a result of any such upsets, releases, or spills. In the event of future increases in environmental costs, we may be unable to pass on those cost increases to customers. A discharge of hazardous substances or wastes into the environment could, to the extent losses related to the event are not insured, subject us to substantial expense, including both the cost to comply with applicable laws and regulations and to pay fines or penalties that may be assessed and the cost related to claims made by neighboring landowners and other third parties for personal injury or damage to natural resources or property. The Company will attempt to anticipate future regulatory requirements that might be imposed and plan accordingly to comply with changing

environmental laws and regulations and to minimize costs with respect to more stringent future laws and regulations of more rigorous enforcement of existing laws and regulations.

Hazardous Substance and Waste. To a large extent, the environmental laws and regulations affecting the Company’s operations relate to the release of hazardous substances or solid wastes into soils, groundwater and surface water, and include measures to prevent and control pollution. These laws and regulations generally regulate the generation, storage, treatment, transportation and disposal of solid and hazardous wastes, and may require investigatory and corrective actions at facilities where such waste may have been released or disposed. For instance, the Comprehensive Environmental Response, Compensation and Liability Act, or CERCLA, also known as the “Superfund” law, and comparable state laws, impose liability without regard to fault or the legality of the original conduct, on certain classes of persons that contributed to a release of “hazardous substance” into the environment. Potentially liable persons include the owner or operator of the site where a release occurred and companies that disposed or arranged for the disposal of the hazardous substances found at the site. Under CERCLA, these persons may be subject to joint and several liability for the costs of cleaning up the hazardous substances that have been released into the environment, for damages to natural resources, and for the costs of certain health studies. CERCLA also authorizes the EPA and, in some cases, third parties to take actions in response to threats to the public health or the environment and to seek to recover from the potentially responsible classes of persons the costs they incur. The Company has not received any notification that it may be potentially responsible for cleanup costs under CERCLA or any analogous federal or state laws, except as expressly provided herein.

We also generate, and may in the future generate, both hazardous and nonhazardous solid wastes that are subject to requirements of the federal Resource Conservation and Recovery Act, or RCRA, and/or comparable state statutes. From time to time, the Environmental Protection Agency, or EPA, and state regulatory agencies have considered the adoption of stricter disposal standards for nonhazardous wastes, including crude oil and natural gas wastes. Moreover, it is possible that some wastes generated by us that are currently classified as nonhazardous may in the future be designated as “hazardous wastes,” resulting in the wastes being subject to more rigorous and costly management and disposal requirements.

Air Emissions. The Company’s current and future operations are subject to the federal Clean Air Act and comparable state laws and regulations. These laws and regulations regulate emissions of air pollutants from various industrial sources, including our facilities, and impose various monitoring and reporting requirements. Pursuant to these laws and regulations, we may be required to obtain environmental agency pre-approval for the construction or modification of certain projects or facilities expected to produce air emissions or result in an increase in existing air emissions, obtain and comply with the terms of air permits, which include various emission and operational limitations, or use specific emission control technologies to limit emissions. The Company will likely be required to incur certain capital expenditures in the future for air pollution control equipment in connection with maintaining or obtaining governmental approvals addressing air-emission related issues. Failure to comply with applicable air statutes or regulations may lead to the assessment of administrative, civil or criminal penalties, and may result in the limitation or cessation of construction or operation of certain air emission sources. We believe such requirements will not have a material adverse effect on our financial condition or operating results, and the requirements are not expected to be more burdensome to us than any similarly situated company.

Climate Change. In response to concerns suggesting that emissions of certain gases, commonly referred to as “greenhouse gases” (including carbon dioxide and methane), may be contributing to warming of the Earth’s atmosphere, the U.S. Congress is actively considering legislation to reduce such emissions. In addition, at least one-third of the states, either individually or through multi-state regional initiatives, have already taken legal measures intended to reduce greenhouse gas emissions, primarily through the planned development of greenhouse gas emission inventories and/or greenhouse gas cap and trade programs. In addition, EPA is taking steps that would result in the regulation of greenhouse gases as pollutants under the federal Clean Air Act. Furthermore, in September 2009 the EPA finalized regulations that require monitoring and reporting of greenhouse gas emissions on an annual basis including extensive greenhouse gas monitoring and reporting requirements beginning in 2010. Although the greenhouse gas reporting rule does not control greenhouse gas emission levels from any facilities, it will still cause us to incur monitoring and reporting costs for emissions that are subject to the rule. Some of our facilities include source categories that are subject to the greenhouse gas reporting requirements included in the final rule. In December 2009 the EPA also issued findings that greenhouse gases in the atmosphere endanger public health and welfare and emissions from mobile sources cause or contribute to greenhouse gases in the atmosphere. The endangerment findings will not immediately affect our operations, but standards eventually promulgated pursuant to these findings could affect our operations and ability to obtain air permits for new or modified facilities.

Legislation and regulations relating to control or reporting of greenhouse gas emissions are also in various stages of discussions or implementation in about one-third of the states. Lawsuits have been filed seeking to force the federal government to regulate greenhouse gases emissions under the Clean Air Act and to require individual companies to reduce greenhouse gas emissions from their operations. These and other lawsuits may result in decisions by state and federal courts and agencies that could impact the Company’s operations and ability to obtain certifications and permits to construct future projects.

Passage of climate change legislation or other federal or state legislative or regulatory initiatives that regulate or restrict emissions of greenhouse gases in areas in which we conduct business could adversely affect the demand for the products we store, transport, and process, and depending on the particular program adopted, could increase the costs of our operations including costs to operate and maintain our facilities, install new emission controls on our facilities, acquire allowances to authorize the Company’s greenhouse gas emissions, pay any taxes related to the Company’s greenhouse gas emissions and/or administer and manage a greenhouse gas emissions program. We may be unable to recover any such lost revenues or increase costs in the rates we charge customers, and any such recovery may depend on events beyond our control. Reductions in our revenues or increases in our expenses as a result of climate control initiatives could have adverse effects on the Company’s business, financial position, results of operations and prospects.

Clean Water Act. The Federal Water Pollution Control Act, also known as the Clean Water Act, and comparable state laws impose restrictions and strict controls regarding the discharge of pollutants, including natural gas liquid related wastes, into state waters or waters of the United States. Regulations promulgated pursuant to these laws require that entities that discharge into federal and state waters obtain National Pollutant Discharge Elimination System, or NPDES, and/or state permits authorizing these discharges. The Clean Water Act and analogous state laws assess administrative, civil and criminal penalties for discharges of unauthorized pollutants into the water and impose substantial liability for the costs of removing spills from such waters. In addition, the Clean Water Act and analogous state laws require that individual permits or coverage under general permits be obtained by covered facilities for discharges of storm water runoff. The Company believes that it is in substantial compliance with Clean Water Act permitting requirements as well as the conditions imposed there under, and that continued compliance with such existing permit conditions will not have a material effect on the Company’s operations.

TCEQ. In 1993 during remediation of a small spill area, the Texas Commission on Environmental Quality (TCEQ) required South Hampton to drill a well to check for groundwater contamination under the spill area. Two pools of hydrocarbons were discovered to be floating on the groundwater at a depth of approximately 25 feet. One pool is under the site of a former gas processing plant owned and operated by Sinclair, Arco and others before its purchase by South Hampton in 1981. Analysis of the material indicates it entered the ground prior to South Hampton’s acquisition of the property. The other pool is under the original South Hampton facility and analysis indicates the material was deposited decades ago. Tests conducted have determined that the hydrocarbons are contained on the property and not migrating in any direction. The recovery process was initiated in June 1998 and approximately $53,000 was spent setting up the system. The recovery is proceeding as planned and is expected to continue for many years until the pools are reduced to acceptable levels. Expenses of recovery and periodic migration testing are being recorded as normal operating expenses. Expenses for future recovery are expected to stabilize and be less per annum than the initial set up cost, although there is no assurance of this effect. The light hydrocarbon recovered from the former gas plant site is compatible with our normal Penhex feedstock and is accumulated and transferred into the Penhex feedstock tank. The material recovered from under the original South Hampton site is accumulated and sold as a by-product. Approximately 75 barrels were recovered during 2011 and 150 barrels during 2010. The recovered material had an economic value of approximately $8,000 during 2011 and $13,000 during 2010. Consulting engineers estimate that as much as 20,000 barrels of recoverable material may be available to South Hampton for use in its process or for sale. At current market values this material, if fully recovered would be worth approximately $2,000,000. The final volume present and the ability to recover it are both highly speculative issues due to the area over which it is spread and the fragmented nature of the pockets of hydrocarbon. South Hampton has drilled additional wells periodically to further delineate the boundaries of the pools and to ensure that migration has not taken place. These tests confirmed that no migration of the hydrocarbon pools has occurred. The TCEQ has deemed the current action plan acceptable and reviews the plan on a semi-annual basis.

The Clean Air Act Amendments of 1990. The Clean Air Act Amendments of 1990 had a positive effect on the Petrochemical Company’s business as manufacturers search for ways to use more environmentally acceptable materials in their processes. There is a current trend among manufacturers toward the use of lighter and more recoverable C5 hydrocarbons (pentanes) which comprise a large part of the Petrochemical Company’s product line. We believe our

ability to manufacture high quality solvents in the C5 hydrocarbon market will provide a basis for growth over the coming years. Also, as the use of C6 solvents is phased out in parts of the industry, several manufacturers of such solvents have opted to no longer market those products. As the number of producers has consolidated, we have increased our market share at higher sales prices from customers who still require C6 solvents in their business.

As discussed above under “United States Mineral Interests” in 2008 the Company learned of a claim by the BLM against World Hydrocarbons, Inc. for contamination of real property owned by the BLM north of and immediately adjacent to the processing mill situated on property owned by PEVM. World Hydrocarbons, Inc. responded to the BLM by stating that it does not own the mill and that PEVM is the owner and responsible party.

The number of regular employees was approximately 160, 145 and 140 at years ended 2011, 2010 and 2009, respectively. Regular employees are defined as active executive, management, professional, technical and wage employees who work full time or part time for the Company and are covered by our benefit plans and programs.

During 2010 we either terminated or transferred to AMAK all of our employees working in Saudi Arabia except for 2 who were subsequently terminated early in 2011. In connection therewith, we paid accrued salaries and termination benefits due these employees with the exception of Mr. Hatem El Khalidi whose termination benefits were accrued pending resolution of lawsuits brought by Mr. El Khalidi against the Company in Saudi Arabia and the United States. See Item 3. Legal Proceedings. Mr. Ghazi Sultan, a director of the Company, is acting as the Company’s representative in Saudi Arabia.

The petrochemical and mining industries are highly competitive. There is competition within the industries and also with other industries in supplying the chemical and mineral needs of both industrial and individual consumers. We compete with other firms in the sale or purchase of needed goods and services and employ all methods of competition which are lawful and appropriate for such purposes. See further discussion under “Intense competition” in Item 1a.

We own a 37% interest in AMAK, a Saudi Arabian closed joint stock mining company. AMAK’s mining activities are expected to produce copper, zinc, gold, silver, and possibly nickel. The AMAK project, which encompasses the Al Masane mine, processing plant and ancillary facilities is located in Najran province in southwestern Saudi Arabia. Specifically, it is located 75 km northwest of the city of Najran, the provincial capital and midway between the outpost of Rihab and the district town of Sufah.

In August 2010 the Saudi Arabian Ministry of Commerce approved amendments to AMAK’s Articles of Association and Bylaws which provide that the Company fully and completely paid the subscription price for 18,450,000 shares of AMAK stock (or 41% of the issued and outstanding shares), that neither AMAK nor the other AMAK shareholders may require the Company to make an additional capital contribution without the Company’s written consent, and that the Company will retain seats on the AMAK Board equal in number to that of the Saudi Arabian shareholders for a three year period beginning August 25, 2009. This was the final step in settling the issue as to whether the Company might be obligated to make an additional capital contribution to AMAK.

On October 24, 2010, we executed a limited Guarantee in favor of the Saudi Industrial Development Fund ("SIDF") guarantying up to 41% of the SIDF loan to AMAK in the principal amount of 330,000,000 Saudi Riyals (US$88,000,000) (the "Loan"). As a condition of the Loan, SIDF required all shareholders of AMAK to execute personal or corporate Guarantees totaling 162.55% of the overall Loan amount. The other AMAK shareholders provided personal Guarantees. We were the only AMAK sharehodler providing a corporate Guarantee. The Loan was required in order for AMAK to fund construction of the underground and above-ground portions of its mining project in southwest Saudi Arabia and to provide working capital for commencement of operations.

In July 2011 we announced that the Arab Mining Company (ARMICO) invested US $37.3 million, acquiring five million shares or 10% interest in AMAK. This capital provided AMAK with the financing necessary to start full production. ARMICO acquired a seat on AMAK's board which is held by Mr. Sultan Al-Shawli, Saudi Deputy Minister for Petroleum and Minerals. Mr. Al-Shawli's election increases the total number of board members to nine.

ARMICO paid 28 Saudi Riyals per share for their 10% stake in the AMAK joint stock company. AMAK's Saudi partners now own 53%, and we own 37%.

Accounting Treatment of Investment in AMAK. Initially, we accounted for our investment in AMAK using the equity method of accounting under the presumption that since we owned more than 20% of AMAK, we would have the ability to exercise significant influence over the operating and financial policies of AMAK. AMAK’s bylaws require that audited financial statements for each year ended December 31 be submitted to its stockholders by June 30 of the following year. As a result, we expected to obtain the audited financial statements of AMAK by June 30, 2009, and in addition we expected to be able to secure the cooperation of AMAK and its auditors in converting those financial statements from generally accepted accounting principles in Saudi Arabia (“Saudi GAAP”) to U.S. generally accepted accounting principles (“U.S. GAAP”). However, by August 2009, no financial statements of AMAK were produced. In May 2010 we received a draft of the 2009 financial statements of AMAK prepared under Saudi GAAP. At that time we introduced a resolution at a meeting of the AMAK Board of Directors that would require AMAK to produce annual and quarterly financial statements prepared in accordance with U.S. GAAP which the Company required in order to apply the equity method of accounting for the investment. The resolution was defeated as the result of the casting of the tie breaking vote held by the Saudi Chairman of the Board. Consequently, we concluded that since August 2009 we no longer had significant influence over the operating and financial policies of AMAK and changed to the cost method of accounting for our investment in AMAK. We recorded our cost method investment in AMAK at the carrying amount of its equity method investment at the date the method of accounting was changed. Also see Item 1A – Risk Factors - Inability to significantly influence AMAK activities.”

Going forward, the lack of ability to exert significant influence basically means that we hold a passive ownership interest in AMAK. The AMAK Saudi directors have taken the lead in dealing with: (i) various contractors who are constructing the underground and above ground mining facilities, (ii) personnel issues, (iii) credit facilities from third party lenders, and (iv) consultants assisting in various phases of mine development. The Company believes that it has developed a good working relationship with the other AMAK stockholders and feels comfortable with allowing the AMAK Saudi directors to oversee the operation, especially since the project is located in their region and they are better qualified to deal with cultural issues and other unique aspects of doing business in Saudi Arabia. Periodically we make suggestions as to how the operation could be improved and generally the AMAK Saudi directors have been receptive to those ideas.

Cash Flows from AMAK. Our investment in AMAK will produce cash flows to the Company at such time as AMAK pays dividends. The Company anticipates that AMAK may have the ability to begin paying dividends once it has commenced commercial operations, and cash flows from those operations are sufficient to pay dividends after AMAK first services its $88 million credit facility and AMAK’s Board of Directors sets aside cash for required statutory reserves and any other reserves its Board of Directors believes are necessary and appropriate. Since we have no significant influence over AMAK’s Board of Directors, the amount and timing of dividends we receive from AMAK will be controlled by the other investors in AMAK.

AMAK will nonetheless not begin paying any dividends until it has commenced commercial production and achieved positive operating cash flows. AMAK successfully completed the construction phase of the mine and turned the facility over to the surface facility operator on November 28, 2011. Metal concentrates will be trucked to the Port of Jizan and stored until such time as there are quantities sufficient to fill a cargo ship. Once the mine reaches full capacity, several vessels per year will be loaded with copper and zinc concentrates which can then be shipped worldwide. In an effort to improve cash flow, AMAK is in discussions concerning an advanced payment covenant with its marketing agent, Ocean Partners, and may receive up to 80 percent of the market value for metal concentrates in 1,000 ton increments when stored in a secure area within the mill.

As a result of the foregoing, we do not anticipate receiving any substantial cash flows from our investment in AMAK until 2013 at the earliest, and there can be no assurance as to the amount or timing of any cash flows we will receive from our investment in AMAK.

We assess our investment in AMAK for impairment when events are identified, or there are changes in circumstances that may have an adverse effect on the fair value of the investment. We consider recoverable ore reserves and the amount and timing of the cash flows to be generated by the production of those reserves, as well as, recent equity transactions within AMAK.

The Company will provide paper copies of this Annual Report on Form 10-K, our quarterly reports on Form 10-Q, our current reports on Form 8-K and amendments to those reports, all as filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, free of charge upon written or oral request to Arabian American Development Company, P. O. Box 1636, Silsbee, TX 77656, (409) 385-8300. These reports are also available free of charge on our website, www.arabianamericandev.com, as soon as reasonably practicable after they are filed electronically with the SEC. South Hampton also has a website at www.southhamptonr.com, and AMAK has a website at www.amak.com.sa. These websites and the information contained on or connected to them are not incorporated by reference herein to the SEC filings.

The Company’s financial and operating results are subject to a variety of risks inherent in the global petrochemical and mining businesses (due to our investment in AMAK). Many of these risk factors are not within our control and could adversely affect our business, our financial and operating results or our financial condition. We discuss some of those risks in more detail below.

Use of single source suppliers for raw materials could create supply issues

The Company’s use of single source suppliers for certain raw materials could create supply issues. Replacing a single source supplier could delay production of some products as replacement suppliers initially may be subject to capacity constraints or other output limitations. The loss of a single source supplier, the deterioration of our relationship with a single source supplier, or any unilateral modification to the contractual terms under which we are supplied raw materials by a single source supplier could adversely affect our revenue and gross margins.

Dependence on a limited number of customers could adversely impact profitability

During 2011, 2010 and 2009, sales to each of two customers by the Petrochemical Company exceeded 10 percent or more of the Company’s revenues. In both cases these sales represented multiple products at multiple facilities. The total loss of either of these two customers could adversely affect the Petrochemical Company’s ability to market its products on a competitive basis and generate a profit.

Varying economic conditions could adversely impact demand for products

The demand for petrochemicals and metals correlates closely with general economic growth rates. The occurrence of recessions or other periods of low or negative growth will typically have a direct adverse impact on our results. Other factors that affect general economic conditions in the world or in a major region, such as changes in population growth rates or periods of civil unrest, also impact the demand for petrochemicals and metals. Economic conditions that impair the functioning of financial markets and institutions also pose risks to the Company, including risks to the safety of our financial assets and to the ability of our partners and customers to fulfill their commitments to the Company. In addition, the revenue and profitability of our operations have historically varied, which makes future financial results less predictable. The Company’s revenue, gross margin and profit vary among our products, customer groups and geographic markets; and therefore, will likely be different in future periods than currently. Overall gross margins and profitability in any given period are dependent partially on the product, customer and geographic mix reflected in that period’s net revenue. In addition, newer geographic markets may be relatively less profitable due to investments associated with entering those markets and local pricing pressures. Market trends, competitive pressures, increased raw material or shipping costs, regulatory impacts and other factors may result in reductions in revenue or pressure on gross margins of certain segments in a given period which may necessitate adjustments to our operations.

Environmental regulation

The petrochemical industry is subject to extensive environmental regulation pursuant to a variety of federal and state regulations. Such environmental legislation imposes, among other things, restrictions, liabilities and obligations in connection with storage, transportation, treatment and disposal of hazardous substances and waste. Legislation also requires us to operate and maintain our facilities to the satisfaction of applicable regulatory authorities. Costs to comply with these regulations are significant to our business. Failure to comply with these laws or failure to obtain permits may expose us to fines, penalties or interruptions in operations that could be material to our results of operations.

Safety, business controls and environmental risk management

Our results depend upon management’s ability to minimize the inherent risks of petrochemical operations, to control effectively our business activities and to minimize the potential for human error. We apply rigorous management systems and continuous focus to workplace safety and to avoid spills or other adverse environmental events. Substantial liabilities and other adverse impacts could result if our systems and controls do not function as intended. Business risks also include the risk of cyber security breaches. If our systems for protecting against cyber security risks prove to be insufficient, we could be adversely affected by having our business systems compromised, our proprietary information altered, lost or stolen, or our business operations disrupted.

Regulatory and litigation

Even in countries with well-developed legal systems where the Company does business, we remain exposed to changes in law that could adversely affect our results, such as increases in taxes, price controls, changes in environmental regulations or other laws that increase our cost of compliance, and government actions to cancel contracts or renegotiate items unilaterally. We may also be adversely affected by the outcome of litigation or other legal proceedings, especially in countries such as the United States in which very large and unpredictable punitive damage awards may occur. AMAK’s mining lease for the Al Masane area in Saudi Arabia is subject to the risk of termination if AMAK does not comply with its contractual obligations. Further, our investment in AMAK is subject to the risk of expropriation or nationalization. If a dispute arises, the Company may have to submit to the jurisdiction of a foreign court or panel or may have to enforce the judgment of a foreign court or panel in that foreign jurisdiction. Because of our substantial international investment, our business is affected by changes in foreign laws and regulations (or interpretation of existing laws and regulations) affecting both the mining and petrochemical industries, and foreign taxation. The Company will be directly affected by the adoption of rules and regulations (and the interpretations of such rules and regulations) regarding the exploration and development of mineral properties for economic, environmental and other policy reasons. We may be required to make significant capital expenditures to comply with non-U.S. governmental laws and regulations. It is also possible that these laws and regulations may in the future add significantly to our operating costs or may significantly limit our business activities. Additionally, the Company’s ability to compete in the international market may be adversely affected by non-U.S. governmental regulations favoring or requiring the awarding of leases, concessions and other contracts or exploration licenses to local contractors or requiring foreign contractors to employ citizens of, or purchase supplies from, a particular jurisdiction. We are not currently aware of any specific situations of this nature, but there are always opportunities for this type of difficulty to arise in the international business environment.

Loss of key personnel and management effectiveness

In order to be successful, we must attract, retain and motivate executives and other key employees including those in managerial, technical, sales, and marketing positions. We must also keep employees focused on our strategies and goals. The failure to hire or loss of key employees could have a significant adverse impact on operations. An important component of our competitive performance is our ability to operate efficiently including our ability to manage expenses and minimize the production of low margin products on an on-going basis. This requires continuous management focus including technological improvements, cost control and productivity enhancements. The extent to which we manage these factors will impact our performance relative to competition. For projects in which we are not in control (such as the AMAK mining project) we depend on the managerial effectiveness of one or more co-investors whom we do not control.

Market place volatility

The Company’s stock price, like that of other companies, can be volatile. Some of the factors that can affect our stock price are:

|

•

|

Speculation in the press or investment community about, or actual changes in, our executive team, strategic position, business, organizational structure, operations, financial condition, financial reporting and results, effectiveness of cost cutting efforts, prospects or extraordinary transactions;

|

|

•

|

Announcements of new products, services, technological innovations or acquisitions by the Company or competitors; and

|

|

•

|

Quarterly increases or decreases in revenue, gross margin or earnings, changes in estimates by the investment community or guidance provided by the Company, and variations between actual and estimated financial results.

|

General or industry-specific market conditions or stock market performance or domestic or international macroeconomic and geopolitical factors unrelated to our performance may also affect the price of our common stock. For these reasons, investors should not rely on recent trends to predict future stock prices, financial condition, results of operations or cash flows. In addition, following periods of volatility in a company’s securities, securities class action litigation against a company is sometimes instituted. If instituted against us, this type of litigation, while insured against monetary awards and defense cost, could result in substantial diversion of management’s time and resources.

Risk associated with extraordinary transactions

As part of the Company’s business strategy, we sometimes engage in discussions with third parties regarding possible investments, acquisitions, strategic alliances, joint ventures, divestitures and outsourcing transactions (“extraordinary transactions”) and enter into agreements relating to such extraordinary transactions in order to further our business objectives. In order to pursue this strategy successfully, we must identify suitable candidates for and successfully complete extraordinary transactions, some of which may be large and complex, and manage post-closing issues such as the integration of acquired companies or employees. Integration and other risks of extraordinary transactions can be more pronounced for larger and more complicated transactions, or if multiple transactions are pursued simultaneously. If the Company fails to identify and complete successfully extraordinary transactions that further our strategic objectives, we may be required to expend resources to develop products and technology internally, we may be at a competitive disadvantage or we may be adversely affected by negative market perceptions, any of which may have a material adverse effect on the Company’s revenue, gross margin and profitability. Integration issues are complex, time-consuming and expensive and, without proper planning and implementation, could significantly disrupt our business. The challenges involved in integration include:

|

•

|

Combining product offerings and entering into new markets in which we are not experienced;

|

|

•

|

Convincing customers and distributors that the transaction will not diminish client service standards or business focus, preventing customers and distributors from deferring purchasing decisions or switching to other suppliers (which could result in our incurring additional obligations in order to address customer uncertainty), and coordinating sales, marketing and distribution efforts;

|

|

•

|

Minimizing the diversion of management attention from ongoing business concerns;

|

|

•

|

Persuading employees that business cultures are compatible, maintaining employee morale and retaining key employees, engaging with employee works councils representing an acquired company’s non-U.S. employees, integrating employees into the Company, correctly estimating employee benefit costs and implementing restructuring programs;

|

|

•

|

Coordinating and combining administrative, manufacturing, and other operations, subsidiaries, facilities and relationships with third parties in accordance with local laws and other obligations while maintaining adequate standards, controls and procedures;

|

|

•

|

Achieving savings from supply chain integration; and

|

|

•

|

Managing integration issues shortly after or pending the completion of other independent transactions.

|

The Company periodically evaluates and enters into significant extraordinary transactions on an ongoing basis. We may not fully realize all of the anticipated benefits of any extraordinary transaction, and the timeframe for achieving benefits of an extraordinary transaction may depend partially upon the actions of employees, suppliers or other third parties. In addition, the pricing and other terms of our contracts for extraordinary transactions require us to make estimates and assumptions at the time we enter into these contracts, and, during the course of our due diligence, we may not identify all of the factors necessary to estimate our costs accurately. Any increased or unexpected costs, unanticipated delays or failure to achieve contractual obligations could make these agreements less profitable or unprofitable. Managing extraordinary transactions requires varying levels of management resources, which may divert our attention from other business operations. These extraordinary transactions also have resulted and in the future may result in significant costs and expenses and charges to earnings. Moreover, the Company has incurred and will incur additional depreciation and

amortization expense over the useful lives of certain assets acquired in connection with extraordinary transactions, and, to the extent that the value of goodwill or intangible assets with indefinite lives acquired in connection with an extraordinary transaction becomes impaired, we may be required to incur additional material charges relating to the impairment of those assets. In order to complete an acquisition, we may issue common stock, potentially creating dilution for existing stockholders, or borrow, affecting our financial condition and potentially our credit ratings. Any prior or future downgrades in the Company’s credit rating associated with an acquisition could adversely affect our ability to borrow and result in more restrictive borrowing terms. In addition, the Company’s effective tax rate on an ongoing basis is uncertain, and extraordinary transactions could impact our effective tax rate. We also may experience risks relating to the challenges and costs of closing an extraordinary transaction and the risk that an announced extraordinary transaction may not close. As a result, any completed, pending or future transactions may contribute to financial results that differ from the investment community’s expectations in a given quarter.

Guaranteeing Performance by Others including Third Parties and Others

From time to time, the Company may be required or determine it is advisable to guarantee performance of loan agreements by others in which the Company maintains a financial interest. In such instances, if the primary obligor is unable to perform its obligations, the Company might be forced to perform the primary obligor’s obligations which could negatively impact the Company’s financial interests.

Economic and Political Instability; Terrorist Acts; War and Other Political Unrest

The U.S. military action in Iraq and Afghanistan, the terrorist attacks that took place in the United States on September 11, 2001, the potential for additional future terrorist acts and other recent events, including terrorist related activities and civil unrest in Egypt, Yemen, Libya, Bahrain and Syria, the on-going Iranian nuclear confrontation, as well as the European debt crisis, have caused uncertainty in the world’s financial markets and have significantly increased global political, economic and social instability, including in Saudi Arabia, a country in which we have a substantial investment. It is possible that further acts of terrorism may be directed against the United States domestically or abroad, and such acts of terrorism could be directed against our investment in those locations. Such economic and political uncertainties may materially and adversely affect our business, financial condition or results of operations in ways that cannot be predicted at this time. Although it is impossible to predict the occurrences or consequences of any such events, they could result in a decrease in demand for our products, make it difficult or impossible to deliver products to our customers or to receive components from our suppliers, create delays and inefficiencies in our supply chain and result in the need to impose employee travel restrictions. We are predominantly uninsured for losses and interruptions caused by terrorist acts, conflicts and wars. Our future revenue, gross margin, expenses and financial condition also could suffer due to a variety of international factors, including:

|

•

|

Ongoing instability or changes in a country’s or region’s economic or political conditions, including inflation, recession, interest rate fluctuations and actual or anticipated military or political conflicts;

|

|

•

|

Longer accounts receivable cycles and financial instability among customers;

|

|

•

|

Trade regulations and procedures and actions affecting production, pricing and marketing of products;

|

|

•

|

Local labor conditions and regulations;

|

|

•

|

Geographically dispersed workforce;

|

|

•

|

Changes in the regulatory or legal environment;

|

|

•

|

Differing technology standards or customer requirements;

|

|

•

|

Import, export or other business licensing requirements or requirements relating to making foreign direct investments, which could affect our ability to obtain favorable terms for labor and raw materials or lead to penalties or restrictions;

|

|

•

|

Difficulties associated with repatriating cash generated or held abroad in a tax-efficient manner and changes in tax laws; and

|

|

•

|

Fluctuations in freight costs and disruptions in the transportation and shipping infrastructure at important geographic points of exit and entry for our products and shipments.

|

Currency fluctuations

Currency variations also contribute to fluctuations in sales of products and services in impacted jurisdictions. In addition, currency variations can adversely affect margins on sales of our products in countries outside of the United States.

Business disruption

Business disruptions could harm the Company’s future revenue and financial condition and increase our costs and expenses. Our operations could be subject to earthquakes, power shortages, telecommunications failures, water shortages, tsunamis, floods, hurricanes, typhoons, fires, extreme weather conditions, medical epidemics and other natural or manmade disasters or business interruptions, for some of which we may be self-insured. The occurrence of any of these business disruptions could harm our revenue and financial condition and increase our costs and expenses.

Dependence on AMAK management and Board

We are relying upon AMAK’s management and Board to employ various respected engineering and financial advisors to assist in the development and evaluation of the mining projects in Saudi Arabia. During 2011 AMAK utilized the services Behre Dolbear of London for ongoing guidance regarding construction, turn over and eventual operation of the ore-processing and underground facilities, and other items to ensure success of the project. Additionally, AMAK hired two very experienced persons in 2011 to serve as Chief Executive Officer and Chief Financial Officer. The amount of risk will ultimately depend upon the AMAK’s ability to use consultants and experienced personnel to manage the operation in Saudi Arabia.

Inability to significantly influence AMAK activities

We do not have the ability to significantly influence AMAK activities for a number of reasons including disputed terms of organizational documents which diluted our ownership percentage, inability to persuade the remaining board members regarding certain management decisions, lack of control at the board of director level, cultural differences, differing accounting and management practices, differing governmental laws and regulations, and the fact that the AMAK mining project is halfway around the world from the Company’s main base of operations in the United States.

Inability to recoup investment in AMAK

The Company will only recover its investment in AMAK through either the receipt of dividends from AMAK or the sale of part or all of its interest in AMAK. There is a risk that we will be unable to recover our investment in AMAK if AMAK is not profitable, or if AMAK’s Board of Directors chooses not to declare dividends even if AMAK is profitable. However, since the Company has no significant influence over AMAK’s Board of Directors, the amount and timing of the dividends we receive from AMAK will be controlled by the other investors in AMAK. With respect to the sale of part or all of our interest in AMAK, under Saudi law, AMAK must sell a portion of its equity to the public once AMAK has been profitable for two years. While the proceeds of such a sale might allow the Company to recover its investment in AMAK, there is no assurance that AMAK will achieve the profitability required for such a public sale, or that the market conditions for any such public sale will be favorable enough to allow us to recover our investment.

AMAK’s inability to obtain sufficient funding

In the event AMAK is unable to continue to borrow funds in an amount sufficient to fund operations, AMAK may be forced to take other less desirable methods to raise necessary capital such as selling additional equity in AMAK at a possible discount, operations could cease and the newly constructed assets could sit unused and deteriorate over time, or worst case the AMAK shareholders could lose their investment or be forced to sell for a significant loss.

AMAK’s inability to obtain additional mining leases

In the event AMAK is unable to obtain additional mining leases, there would be a loss of future opportunities.

Cancellation of the current mining lease held by AMAK

In the event that the Saudi Ministry cancels the current lease, AMAK shareholders including the Company could lose their investment or be forced to sell for a loss.

Intense competition

The Company competes in the petrochemical industry. Accordingly, we are subject to intense competition among a large number of companies, both larger and smaller than us, many of which have financial capability, facilities, personnel and other resources greater than us. In the specialty products and solvents markets, the Petrochemical Company has one principal competitor in North America, ConocoPhillips. Multiple competitors exist when searching for new business in other parts of the world. We compete primarily on the basis of performance, price, quality, reliability, reputation, distribution, service, and account relationships. If our products, services, support and cost structure do not enable us to compete successfully based on any of those criteria, our operations, results and prospects could be harmed. The Company has a portfolio of businesses and must allocate resources across these businesses while competing with companies that specialize in one or more of these product lines. As a result, we may invest less in certain areas of our businesses than competitors do, and these competitors may have greater financial, technical and marketing resources available to them than our businesses that compete against them. Industry consolidation may also affect competition by creating larger, more homogeneous and potentially stronger competitors in the markets in which we compete, and competitors also may affect our business by entering into exclusive arrangements with existing or potential customers or suppliers. We may have to continue to lower the prices of many of our products and services to stay competitive, while at the same time, trying to maintain or improve revenue and gross margin.

Research and Development

If the Company cannot continue to develop, manufacture and market products and services that meet customer requirements, its revenue and gross margin may suffer. We must make long-term investments and commit significant resources before knowing whether our predictions will accurately reflect customer demand for products and services. After we develop a product, we must be able to manufacture appropriate volumes quickly and at competitive costs. In the course of conducting business, the Company must adequately address quality issues associated with our products and services. In order to address quality issues, we work extensively with our customers and suppliers to determine the cause of the problem and to determine appropriate solutions. However, we may have limited ability to control quality issues. If the Company is unable to determine the cause or find an appropriate solution, it may delay shipment to customers, which would delay revenue recognition and could adversely affect our revenue and reported results. Finding solutions to quality issues can be expensive, adversely affecting our profits. If new or existing customers have difficulty utilizing our products, our operating margins could be adversely affected, and we could face possible claims if we fail to meet customers’ expectations. In addition, quality issues can impair the Company’s relationships with new or existing customers and adversely affect its reputation, which could have a material adverse effect on operating results.

Not Applicable

South Hampton owns and operates a specialty petrochemical facility near Silsbee, Texas which is approximately 30 miles north of Beaumont, Texas, and 90 miles east of Houston. The facility consists of seven operating units which, while interconnected, make distinct products through differing processes: (i) a Penhex Unit; (ii) a Reformer; (iii) a Cyclo-pentane Unit; (iv) an Aromax® Unit; (v) an Aromatics Hydrogenation Unit; (vi) a White Oil Fractionation Unit; and (vii) a Hydrocarbon Processing Demonstration Unit commissioned in 2011 for Gevo. All of these units are currently in operation.

During 2010 we acquired Silsbee Trading and Transportation Company (“STTC”) which owned and operated 14 transport trucks and 23 trailers for delivery of South Hampton’s products. STTC was subsequently merged into South Hampton. South Hampton currently owns 16 trucks and 23 trailers.

Gulf State owns and operates three (3) 8-inch diameter pipelines aggregating approximately 50 miles in length connecting South Hampton’s facility to: (1) a natural gas line, (2) South Hampton’s truck and rail loading terminal and

(3) a major petroleum products pipeline system owned by an unaffiliated third party. All pipelines are operated within Texas Railroad Commission and DOT regulations for maintenance and integrity.

The Company’s only mineral interest in the United States is its ownership interest in PEVM. See Item 1 – Business – United States Mineral Interests.

The Company has a year-to-year lease on space in an office building in Jeddah, Saudi Arabia, used for storage purposes. The Company plans to terminate this lease in 2012.

South Hampton has a leased corporate and sales office in Sugar Land, Texas.

On May 9, 2010, after numerous attempts to resolve certain issues with Mr. Hatem El Khalidi, the Board of Directors terminated the retirement agreement, options, retirement bonuses, and all outstanding directors’ fees due to Mr. El Khalidi, former CEO, President and Director of the Company. In June 2010 Mr. El Khalidi filed suit against the Company in the labor courts of Saudi Arabia alleging additional compensation owed to him for holidays and overtime. In November 2011 the labor court determined that the Company owed Mr. El Khalidi $255,000 for holiday pay and dismissed the remainder of his claims. The Company and Mr. El Khalidi have appealed the decision to the next level. In September 2010 Mr. El Khalidi threatened suit against the Company in the U.S. alleging breach of contract under the above agreements and other claims. In late 2010 the Company filed suit against Mr. El Khalidi in the United States District Court in the Eastern District of Texas, Beaumont Division, seeking a declaratory judgment that all monies allegedly owed to Mr. El Khalidi are terminated (the “Federal Court Case”). On March 21, 2011, Mr. El Khalidi filed suit against the Company in the 14th Judicial District Court of Dallas County, Texas for breach of contract and defamation (the “State Court Case”). On July 1, 2011, the Company and Mr. El Khalidi entered into an agreement to dismiss the Federal Court Case and transfer venue for the State Court Case to Hardin County, Texas. Pursuant to this agreement, the Federal Court Case was dismissed on July 13, 2011, and the State Court Case was transferred to Hardin County, Texas on July 15, 2011. There has been no activity in this matter since transfer to Hardin County, Texas. The Company believes that the claims are unsubstantiated and intends to vigorously defend the case. The liabilities owed to Mr. El Khalidi will remain recorded on the Company’s books until the lawsuits are resolved.

On September 14, 2010, South Hampton received notice of a lawsuit filed in the 58th Judicial District Court of Jefferson County, Texas which was subsequently transferred to the 11th Judicial District Court of Harris County, Texas. The suit alleges that the plaintiff became ill from exposure to asbestos. There are approximately 44 defendants named in the suit. South Hampton has placed its insurers on notice of the claim and plans to vigorously defend the case. No amounts have been accrued for this claim.

On April 14, 2011, and April 27, 2011, South Hampton received notice of three lawsuits filed in Jefferson County, Texas. The suits allege that the plaintiffs became ill from benzene exposure during the employment with Goodyear Tire and Rubber Company, an alleged customer of South Hampton. There are numerous defendants named in the suits. South Hampton has placed its insurers on notice of the claims and plans to vigorously defend the cases.

Not applicable

PART II

The Company’s common stock traded on the Nasdaq Stock Market LLC (“Nasdaq”) during the last two fiscal years under the symbol: ARSD. The following table sets forth the high and low bid prices for each quarter as reported by Nasdaq. The quotations reflect inter-dealer prices, without retail mark-up, mark-down or commission and may not represent actual transactions.

| |

|

Nasdaq

|

|

| |

|

High

|

|

|

Low

|

|

|

Fiscal Year Ended December 31, 2011

|

|

|

|

|

|

|

|

Fourth Quarter ended December 31, 2011

|

|

$ |

10.09 |

|

|

$ |

3.20 |

|

|

Third Quarter ended September 30, 2011

|

|

$ |

4.75 |

|

|

$ |

3.16 |

|

|

Second Quarter ended June 30, 2011

|

|

$ |

4.47 |

|

|

$ |

3.70 |

|

|

First Quarter ended March 31, 2011

|

|

$ |

5.10 |

|

|

$ |

3.65 |

|

| |

|

|

|

|

|

|

|

|

|

Fiscal Year Ended December 31, 2010

|

|

|

|

|

Fourth Quarter ended December 31, 2010

|

|

$ |

4.53 |

|

|

$ |

2.20 |

|

|

Third Quarter ended September 30, 2010

|

|

$ |

2.60 |

|

|

$ |

1.63 |

|

|

Second Quarter ended June 30, 2010

|

|

$ |

3.30 |

|

|

$ |

1.99 |

|

|

First Quarter ended March 31, 2010

|

|

$ |

3.15 |

|

|

$ |

2.14 |

|

At March 8, 2012, there were approximately 565 recorded holders (including brokers’ accounts) of the Company’s common stock. The Company has not paid any dividends since its inception and, at this time, does not have any plans to pay dividends in the foreseeable future. The current lender allows the petrochemical subsidiaries to pay dividends to the parent company of up to 30% of EBITDA. The Petrochemical Company was in compliance with this restriction as of December 31, 2011. See Note 10 to the Consolidated Financial Statements.

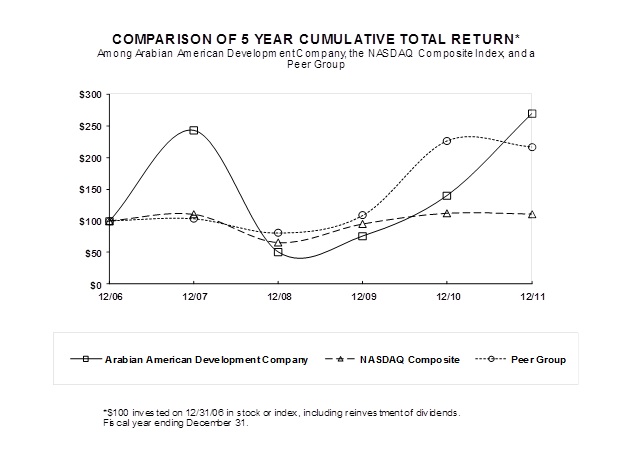

Total Stockholder Return

The following graph compares the cumulative total stockholder return on our common stock against the Nasdaq Composite Index and a Peer Group, for the five years ending December 31, 2011. The graph was constructed on the assumption that $100 was invested in our common stock, the Nasdaq Composite Index and the Peer Group on December 31, 2006, and that any dividends were fully reinvested.

The following is a five-year summary of selected financial data of the Company (in thousands, except per share amounts):

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Revenues

|

|

$ |

199,517 |

|

|

$ |

139,110 |

|

|

$ |

117,587 |

|

|

$ |

154,630 |

|

|

$ |

108,638 |

|

|

Net Income (Loss)

|

|

$ |

8,430 |

|

|

$ |

2,686 |

|

|

$ |

6,627 |

|

|

$ |

(10,731 |

) |

|

$ |

7,771 |

|

|

Net Income (Loss) Per Share-Diluted

|

|

$ |

0.35 |

|

|

$ |

0.11 |

|

|

$ |

0.28 |

|

|

$ |

(0. 46 |

) |

|

$ |

0.33 |

|

|

Total Assets (at December 31)

|

|

$ |

110,612 |

|

|

$ |

92,528 |

|

|

$ |

90,487 |

|

|

$ |

96,290 |

|

|

$ |

84,221 |

|

|

Notes Payable (at December 31)

|

|

$ |

12 |

|

|

$ |

12 |

|

|

$ |

12 |

|

|

$ |

12 |

|

|

$ |

11,012 |

|

|

Current Portion of Long-Term Debt (at December 31)

|

|

$ |

1,500 |

|

|

$ |

1,865 |

|

|

$ |

1,400 |

|

|

$ |

4,920 |

|

|

$ |

31 |

|

|

Total Long-Term Debt Obligations

(at December 31)

|

|

$ |

22,739 |

|

|

$ |

20,836 |

|

|

$ |

23,439 |

|

|

$ |

23,557 |

|

|

$ |

9,078 |

|