Arabian American Development Company

1600 Hwy 6 S, Suite 240

Sugar Land, TX 77478

(409) 385-8300

May 19, 2010

United States Securities and Exchange Commission Via: CMRRR

Division of Corporate Finance

100 F Street, N.E.

Washington, D.C. 20549-4628

Attention: Messrs. H. Roger Schwall and Chris White

Re: Arabian American Development Company

Form 10-K for the Fiscal year Ended December 31, 2008

Filed March 16, 2009

Form 10-Q for the Fiscal Quarter Ended September 30, 2009

Filed November 6, 2009

Response letter dated January 8, 2010

File No. 1-33926

Dear Messrs. Schwall and White:

Please accept this letter as Arabian American Development Company’s (the “Company”) response to your letter dated May 7, 2010.

Form 10-K for the Fiscal Year Ended December 31, 2009

General

|

1.

|

Our comments with regard to the Form 10-K for the fiscal year ended December 31, 2009 are intended to apply to the Form 10-K for the fiscal year ended December 31, 2008, to the extent they are also relevant to such filing.

|

Response: We respectfully request that the staff allow us to implement all of the changes required to respond to its comments in an amendment to our 2009 Form 10-K and that the staff not require us to also amend our 2008 Form 10-K. In support of this request we would point out the following:

|

|

-

|

Form 8-K filed March 11, 2010, included the restated 2008 financial statements and has now been on file for more than two months. That Form 8-K included a statement that the Company’s previously issued 2008 financial statements, as included in its 2008 Form 10-K filed with the SEC on March 16, 2009, should no longer be relied upon.

|

|

|

-

|

The 2009 Form 10-K, which included the restated 2008 financial statements, has now been on file for two full months. That Form 10-K also included a statement (at page 38) to the effect that the 2008 financial statements had been restated, and that the 2008 financial statements, as included in the 2008 Form 10-K, should not be relied upon. Additionally, the 2008 Form 10-K is now 14 months old.

|

|

Messrs. H. Roger Schwall and Chris White

May 19, 2010

Page 2 of 17

|

-

|

In the 2009 Form 10-K we included disclosure (pages 21 and 22) about the unresolved staff comments on our 2008 Form 10-K. In the amended 2009 Form 10-K that we will file at such time as these comments are resolved, we will not remove this disclosure, but we will update it to indicate that the amended Form 10-K reflects revisions which have resolved the comments.

|

In light of the above, we believe that investors are well informed to no longer rely upon the 2008 Form 10-K, in fact are no longer relying on the 2008 Form 10-K, and that a formal amendment to the 2008 Form 10-K would have no affect on investors or other readers.

|

2.

|

Please refer to SEC Release No. 33-9089, Proxy Disclosure Enhancements, and provide us with a draft of enhanced disclosure that complies with the new rules. We may have further comments after reviewing your response.

|

Response: We respectfully note your comment and have attached a draft of a completely rewritten disclosure that we believe complies with SEC Release No. 33-9089 as shown in Attachment A.

Management’s Discussion and Analysis of Financial Condition and Results of Operations, page 29

Liquidity and Capital Resources, page 31

|

3.

|

We reissue comment 7 from our letter dated November 30, 2009 in relevant part. Please disclose in this section your sources of liquidity, including a description of all material terms of the revolving loan agreement and the term loan agreement described in Note 10 to your financial statements. In addition, we note your disclosure at page 38 regarding payments due within three years that relate to contractual obligations. Please disclose your anticipated source of funds for such payments.

|

Response: We respectfully note your comment and will include a description of our revolving loan and term loan agreement described in Note 10 to our financial statements in our amended Form 10-K for the year ended December 31, 2009, as shown in Attachment B. With regard to your comment concerning page 38, we will add the following disclosure underneath the table:

“The anticipated source of funds for payments due within three years that relate to contractual obligations is from a combination of continuing operations and long-term debt refinancing.”

Directors and Executive Officers of the Registrant, page 46

|

4.

|

Please enhance your disclosure so that it includes all of the information required by Item 401 of Regulation S-K. For example, in many of the biographical sketches, information is missing as to specific titles held, specific names of organizations, and exact periods during which the titles were held.

|

Response: We respectfully note your comment and have enhanced our disclosure regarding the Company’s directors and executive officers in our amended Form 10-K for the year ended December 31, 2009 as follows:

Messrs. H. Roger Schwall and Chris White

May 19, 2010

Page 3 of 17

PART III

Item 10. Directors and Executive Officers of the Registrant

The following sets forth the name and age of each director of the Company as of December 31, 2009, the date of his election as a director and all other positions and offices with the Company held by him.

|

Name; Current Positions Held

|

Age

|

Director since

|

Term expires at Annual meeting in

|

|

Hatem El Khalidi

Co-founder and retired President & CEO of the Company

|

85

|

1968

|

2010

|

|

Nicholas N. Carter ………………………………………….

President, Chief Executive Officer of the Company since July 2009, President of the Petrochemical Company since 1987, Member of AMAK Board

|

62

|

2004

|

2011

|

|

Robert E. Kennedy ………………………………………….

Chairman of the Audit and Compensation Committees; Member of Nominating Committee and AMAK Board

|

65

|

2007

|

2012

|

|

Ghazi Sultan

Chairman of the Nominating Committee; Member of Compensation and Audit Committees and AMAK Board

|

73

|

1993

|

2010

|

|

Allen P. McKee

Member of the Audit, Compensation and Nominating Committees and AMAK Board

|

68

|

2009

|

2012

|

|

Mohammed Al Omair

Member of Audit, Compensation and Nominating Committees

|

66

|

2007

|

2011

|

|

Charles W. Goehringer, Jr.

General Counsel

|

51

|

2007

|

2011

|

Mr. Hatem El Khalidi, received a Bachelors Degree in Chemistry from the American University of Beirut in 1946 and a Masters of Science Degree in Geology from Michigan State University in 1950. He was co-founder of the Company in 1967 and served as President from 1975 through June 2009 and Chief Executive Officer of the Company from February 1994 through June 2009. From 1950-55, he was with Geophysical Services, Inc. (later Texas Instruments), Dallas, TX and United Gas Company in Shreveport, LA. From 1956-60, Mr. El Khalidi was Chief Geologist with Yemen Development Corp. seeking oil and mineral concessions in Yemen. From 1960-69, he was a geological consultant with Dallas Resources, operating out of Beirut. Mr. El Khalidi originally discovered the Al Masane ore deposits in 1968 and was granted an exploration license in 1971 and development has been under his direct supervision throughout the life of the project until transferred to AMAK in 2008.

Mr. Nicholas N. Carter, a U.S. citizen and the President and Chief Executive Officer of the Company since July 2009, is a 1975 graduate of Lamar University with a Bachelor of Business Administration Degree in Accounting. Mr. Carter has been a Certified Public Accountant since 1977. He worked at the Sabine River

Messrs. H. Roger Schwall and Chris White

May 19, 2010

Page 4 of 17

Authority of Texas as a Project Accountant from 1973 to 1975. From 1975 to 1977 he was a Staff Accountant with Wathen, DeShong and Company, CPA's. In 1977 he joined South Hampton asController. His job titles with the Company include 1979, Facility Manager at TOCCO, 1982, Treasurer of TOCCO, 1987, President of South Hampton. In 2007 he added the title of Executive Vice President of Arabian American Development Co. in addition to the petrochemical duties. He was named to his current position in 2009 and retains the petrochemical duties. Mr. Carter also serves as a Director and President of Pioche Ely Valley Mines, Inc. of which the Company owns 55% of the outstanding stock. Mr. Carter was appointed to the Board of AMAK in February 2009.

Mr. Robert Kennedy, a U.S. citizen, is the President of Robert E. Kennedy and Associates, a consulting firm assisting various entities with transportation and project development issues in Europe and the Middle East. He has over thirty years experience in the oil and petrochemical industry and retired as General Manager for Supply, Logistics, and Procurement from Chevron Chemical in 2000. During his employment with Chevron he was instrumental in developing the Aromax project in Jubail, Saudi Arabia. Mr. Kennedy holds a Bachelors of Science Degree in Chemical Engineering from the University of Iowa and attended the Masters of Business Administration program of American University. Mr. Kennedy was appointed to the Board of AMAK in 2009. We believe that this experience, as well as his leadership abilities, brings valuable experience and skill to our board of directors.

Mr. Ghazi Sultan, a Saudi citizen, received Bachelor of Science Degrees in Geology and Chemistry from the University of Cairo in 1958. He received a Masters of Science Degree in Geology from the University of Texas in 1964. From 1965-1988, Mr. Sultan served in various Saudi Arabian governmental posts for the Ministry of Petroleum and Minerals, including Director of the Geology Department, Director General of Mineral Resources, Assistant Deputy Minister, and finally as Deputy Minister for Mineral Resources. Mr. Sultan previously served as a member of the Board of Directors of Petromin, the Jeddah Refinery, and King Fahad University of Petroleum and Minerals. He is currently a member of the Board of AMAK. During his career, Mr. Sultan supervised, assisted and negotiated contracts on behalf of the Ministry of Petroleum and Mineral resources with the United States Geological Survey, BRGM of France, Rio – UK Tinto Zinc, British Steel – UK, Roan Selection Trust – UK, Min-Atom – France, Preussag – Germany, Arabian Drilling – Saudi Arabia, and Saudi Sudanese Mission for Red Sea Mining. We believe that his knowledge of the mining industry and manner of conducting business in Saudi Arabia provide a critical resource and skill set to our board of directors.

Mr. Allen P. McKee, a US citizen, appointed to the board in 2009 and subsequently elected to serve until 2012, has an extensive background in investment evaluation and management as well as international finance. He has been an advisor to Fal Holdings Arabia Co. Ltd., Riyadh, since its inception in 1977. Mr. McKee served as president of Montgomery Associates Inc. from 1975-2000, a firm focusing on both venture-stage companies and real property investments. From 1974-78 he was an advisor to companies seeking funding through the International Finance Corp (World Bank Group) and regional development banks. From 1971-74, Mr. McKee served as vice president of Union International (Union Bank’s international venture subsidiary) and previously was investment officer with BankAmerica International Financial Corp. From 1967-70 he was area relations officer on the headquarters staff overseeing the Middle East banking group at Bank of America. He holds a Bachelor of Arts Degree in Economics from the University of Michigan (1964) and a Masters of Business Administration Degree in Finance from the University of California, Berkeley (1971). Mr. McKee served as a naval officer in the US Pacific Fleet from 1964-67. He was appointed to the Board of AMAK in 2009 and serves on the audit, nominations and compensation committees of the Company, chairing the latter. We believe that his knowledge of the Middle East and finance and accounting provide a critical resource and skill set to our board of directors.

Mr. Charles W. Goehringer, Jr., a U.S. citizen and partner of the law firm of Germer Gertz, L.L.P. in Beaumont, Texas, serves as corporate counsel for the Company. From 1981-1987, Mr. Goehringer worked for Gulf States Utilities Company as a mechanical engineer and unit superintendent. From 1987-1995, Mr. Goehringer worked for Quantum Chemical Company as a mechanical engineer and maintenance superintendent. He next worked as an attorney for the law firm of Mehaffy Weber, P.C. from 1995-2000. From 2000 to the present, Mr. Goehringer has been employed as an attorney with the law firm of Germer Gertz, L.L.P. Mr. Goehringer holds a Bachelor of Science Degree in Mechanical Engineering from Lamar

Messrs. H. Roger Schwall and Chris White

May 19, 2010

Page 5 of 17

University, a Masters of Business Administration Degree from Colorado University, and a Doctor of Jurisprudence from South Texas College of Law. Mr. Goehringer also serves as a Director of Pioche ElyValley Mines, Inc. of which the Company owns 55% of the outstanding stock. We believe that his knowledge of the industry and finance provide a critical resource and skill set to our board of directors.

Mr. Mohammed O. Al Omair, a Saudi citizen, resides in Riyadh, Saudi Arabia, and previously served as Senior Vice President & Deputy Chief Executive Officer for Fal Holdings Arabia Co. Ltd. Prior to his service with Fal, he held a senior position with the Gulf Cooperation Counsel (GCC), a six-nation organization of Arab nations in the region. He holds a Bachelor of Arts Degree in Political Science and a Master of Public Administration from the University of Washington. We believe that this experience, as well as his leadership abilities, brings valuable experience and skill to our board of directors.

The Nominating Committee solicits recommendations for potential Board candidates from a number of sources including members of the Board, officers of the Company, individuals personally known to the members of the Board and third-party research. In addition, the Committee will consider candidates submitted by stockholders when submitted in accordance with the procedure described in the Company’s annual proxy statement. The Committee will consider all candidates identified through the processes above and will evaluate each of them on the same basis.

The Board of Directors of the Company has an Audit Committee which is composed of Ghazi Sultan, Mohammed Al Omair, Robert Kennedy and Allen McKee. The Board has determined that each of the members of the Audit Committee meets the Securities and Exchange Commission and Nasdaq Stock Market standards for independence. The Board has also determined that Allen McKee meets the Securities and Exchange Commission criteria of an “audit committee financial expert.”

The following sets forth the name and age of each executive officer of the Company as of December 31, 2009, the date of his appointment and all other positions and offices with the Company held by him.

|

Name

|

Positions

|

Age

|

Appointed

|

|

Nicholas N. Carter

|

President, Chief Executive Officer and Director/President - TOCCO

|

62

|

2009/1987

|

|

Mark Williamson

|

Vice President of Marketing - TOCCO

|

54

|

1996

|

|

Connie Cook

|

Chief Accounting Officer, Secretary, Treasurer/Secretary, Treasurer - TOCCO

|

46

|

2008/2004

|

Each executive officer of the Company serves for a term extending until his successor is elected and qualified.

Please refer to the director discussion above for Mr. Carter’s business experience.

Mr. Mark Williamson is a U.S. Citizen and has been Vice President of Marketing for TOCCO since 1995. Mr. Williamson is a graduate of Sam Houston State University with a BBA in Marketing. Mr. Williamson has been with TOCCO since 1987 and has over 28 years within the petrochemical industry. Before TOCCO, Mr. Williamson spent 5 years with Ashland Chemicals as Sales and Marketing Representative and Branch Manager.

Ms. Connie Cook, a U.S. citizen, received her BBA Degree in Accounting from Lamar University in 1991 and is a CPA. She was the Accounting Manager of TOCCO from 1991-96. She has been the Controller of TOCCO from 1996 to the present and was the Assistant Secretary of TOCCO from 1992-2004. In 2004 Ms. Cook became the Secretary/Treasurer of TOCCO and continues to hold those titles. She was the Assistant Secretary of the Company from 2007-08. In 2008 Ms. Cook became the Secretary/Treasurer of the Company and continues to hold those titles.

Messrs. H. Roger Schwall and Chris White

May 19, 2010

Page 6 of 17

There are no family relationships among our directors and executive officers.

Executive Compensation, page 48

|

5.

|

Please enhance your disclosure so that it includes all of the information required by Item 402 of Regulation S-K. For example:

|

|

|

●

|

You state on page 51 that “In 2009 the Company’s executives received no award based upon 2008 performance.” However, there are awards shown in the “Bonus” column of the Summary Compensation Table. Please explain.

|

Response: We revised the Summary Compensation Table shown in Attachment A in response to this comment to separate South Hampton’s profit sharing program from the Executive Cash Bonus Program. The 2009 awards shown in the “Profit Sharing” column of the revised Summary Compensation Table for Nicholas N. Carter, Connie J. Cook, Mark D. Williamson, Gerardo Maldonado and Marvin Kaufman represent monies paid from South Hampton’s profit sharing plan during 2009, which was available to all South Hampton employees. The 2009 awards shown in the “Bonus” column of the revised Summary Compensation Table for Nicholas N. Carter, Connie J. Cook and Mark D. Williamson represent bonuses totaling $130,000 paid during the first quarter of 2010 under the Executive Cash Bonus Plan. As reflected in the revised Summary Compensation Table, none of the Company’s executives received bonuses under the Executive Cash Bonus Plan, stock grants or stock options in 2009 based upon their 2008 performance, although they along with the other South Hampton employees participated in the South Hampton profit sharing program for 2008. Awards for 2008 shown in the “Restricted Stock Award(s)” column of the revised Summary Compensation Table for Nicholas N. Carter, Connie J. Cook and Mark D. Williamson reflect grants of restricted stock based on the Company’s performance in 2007 that were not issued until the first quarter of 2008.

|

|

●

|

Discuss in your Compensation Discussion and Analysis the grant of the option for 200,000 shares to Mr. El-Khalidi, which is stated in the 2009 Grants of Plan-Based Awards table to have occurred on July 2, 2009. Explain the rationale for this grant.

|

Response: As background, the Board of Directors of the Company adopted the following resolution on October 10, 1995:

|

|

“2. Regarding the accrued retainers of Hatem El-Khalidi, currently about $400,000, which are demand loans to the Company, El-Khalidi shall have the option [the “1995 Option”] to convert any part of these loans outstanding at any time prior to the repayment of these loans into common shares of the Company, at the price of One ($1.00) US dollar per share.” (the “1995 Resolution”)

|

On July 2, 2009, the Board of Directors of the Company discussed the fact that since the Company subsequently paid Mr. El-Khalidi all of the accrued retainers referenced in the 1995 Resolution, the 1995 Option expired by its own terms, and in order to ensure there is no confusion regarding termination of the 1995 Option, the Board adopted the following resolution:

Messrs. H. Roger Schwall and Chris White

May 19, 2010

Page 7 of 17

| |

“RESOLVED that the Option granted by the Company to Hatem El-Khalidi pursuant to the 1995 Resolution is hereby officially terminated in all respects and shall be removed from the Company’s books and records.”

|

The Board of Directors then considered Mr. El-Khalidi’s efforts related to the Al Masane mining project in southwestern Saudi Arabia in conjunction with his retirement as CEO of the Company on June 30, 2009. The Board determined that the Company should issue two options to purchase a total of 400,000 shares to Mr. El-Khalidi, tied to the performance of AMAK.

The rationale for the grant of these two options was based on the fact that virtually all of Mr. El-Khalidi’s career was spent working on the mining project in Saudi Arabia under difficult conditions and the Board believed a substantial award was justified in light of his relatively low salary of $72,000 per annum. However, in order to link the value of that award to the ultimate success of the Saudi Arabia mining project which had been Mr. Khalidi’s focus, the Board of Directors made the options contingent upon the occurrence of the following conditions which are explicitly tied to the performance of AMAK: (i) the first option for 200,000 shares cannot be exercised until such time as the first shipment of ore from the mining project is transported for commercial sale by AMAK and the option terminates if not exercised by June 30, 2012, and (ii) the second option for 200,000 shares cannot be exercised until such time as the Company receives its first cash dividend distribution from AMAK and the option terminates if not exercised by June 30, 2019.

|

|

●

|

We note your statement on page 50 that “The Company includes an annual cash bonus as part of its compensation program because it believes this element of compensation helps to motivate management to achieve key individual and operational objectives by rewarding the achievement of these objectives.” Similarly, on page 52, you state there is “a significant portion of total compensation reflecting a risk aspect tied to long-term and short-term financial and strategic goals.” However, your discussion of “Performance Metrics” on page 52 appears to indicate that the process of determining awards is “subjective” and done after the fact, without pre-established performance metrics. Please explain. Also, your discussion of “Performance Metrics” is limited to the year 2009; accordingly, please add an explanation of the “long-term . . . financial and strategic goals.”

|

Response: We have revised the Compensation Discussion and Analysis section to better describe the process used by the Compensation Committee to determine awards. Please refer to Attachment A. In addition, the Compensation Committee is in the process of requesting proposals from various compensation consultants in the Houston, Texas area for assistance with goal setting and compensation allocation.

Summary Compensation Table, page 53

|

6.

|

You state at page 51 that for 2009 performance, $130,000 in cash and 65,000 in options were awarded and will be paid in the first quarter of 2010. Please advise why the cash portion is not reflected in the Summary Compensation Table with respect to bonus payments earned in 2009. See Item 402(c)(2)(iv) of Regulation S-K.

|

Messrs. H. Roger Schwall and Chris White

May 19, 2010

Page 8 of 17

Response: Pursuant to Item 402(c)(2)(iv) of Regulation S-K, the dollar value of the cash bonuses awarded in 2009, but paid or issued in 2010 will be reflected in the Summary Compensation Table in the amended Form 10-K for the fiscal year ended December 31, 2009.

Review, Approval or Ratification of Transactions with Management and Others, page 60

|

7.

|

Please disclose the standards to be applied by your board when determining whether to approve or ratify related party transactions. See Item 404(b)(1)(ii) of Regulation S-K.

|

Response: Paragraph 18 of the Company’s Amended and Restated Audit Committee Charter, adopted on February 13, 2004, provides: “The Audit Committee, to the extent it deems necessary or appropriate, shall . . . [r]eview and, if appropriate, approve all related party transactions.” See Attachment C-1. At present, the Audit Committee does not have a formal written policy addressing related party transactions. However, in the past, the Audit Committee has handled related party transactions in accordance with the policy outlined in Attachment C-2, which will be placed in front of the Board for adoption at the next scheduled meeting.

Financial Statements

Note 8 – Investment in AMAK, page F-21

|

8.

|

We note your response to prior comment 9 in our letter dated February 23, 2010. Please provide to us your detailed impairment analysis of the assets contributed to AMAK prepared in accordance with ASC 360.10.35-21(f) (SFAS 144, paragraph 8(f)) at the time of the contribution. Your analysis should include the assumptions incorporated by you about the use of the assets and information regarding all other available information used by you in the analysis. Please discuss how your assumptions were determined and how they are consistent with those assumptions used by you to negotiate your joint venture arrangement. If a range was estimated for possible cash flows, tell us how you considered the likelihood of various possible outcomes. We expect that your estimates included cash flows associated with future expenditures necessary to develop the properties, including any interest payments that would be capitalized.

|

We note that depending upon the resolution of the next comment, we would expect you to evaluate impairment in your investment on a regular basis in accordance with the guidance of ASC 325.20.35-2 or 323.10.35-31 and 32 (APB 18), paragraphs 6(a) or 6(b) and 19(h)), as appropriate, ASC 970.323.35-12 (SOP 78-9, p. 20), and related accounting literature.

Response: The assets were contributed to the joint venture on December 30, 2008. In connection therewith an impairment analysis was performed (in actuality, due to the one day gap between the date the assets were contributed and our December 31, 2008 year end, the impairment analysis for the contributed assets was performed at the same time and in conjunction with the general impairment analyses performed as of December 31, 2008). The general impairment analysis found that due to the ongoing creation and organization of the joint venture, and the continuing positive value of the projected cash flow estimates from the project, the assets had actually increased in value rather than suffering an impairment.

Messrs. H. Roger Schwall and Chris White

May 19, 2010

Page 9 of 17

For general background information purposes, in 1994 and 1996 we retained Davy International Canada Ltd. (“Davy”) to review and update the Al Masane Feasibility Study that was prepared by Watts, Griffis and McQuat (“WGM”) in 1982 (excluding the mining portion of the project). The results of Davy’s reviews are contained in the following reports:

|

-

|

Arabian Shield Development Company, Al Masane Project, Saudi Arabia, Feasibility Study for a 2000 TPD Concentrator and Related Infrastructure, Davy Project No. 1313, April 1994; and

|

|

-

|

Arabian Shield Development Company, Al Masane Project, Capital Cost Estimate Update for Concentrator and Related Facilities, Davy Project No. 1432, March 1996.

|

WGM’s reviews are contained in the following reports:

|

-

|

Volumes 1 and 2, Feasibility Study – Al Masane Project – For Arabian Shield Development Company and National Mining Company, WGM, August 27, 1982;

|

|

-

|

Review of the 1982 Feasibility Study – Al Masane Project – For Arabian Shield Development Company and National Mining Company, WGM, September 26, 1984;

|

|

-

|

Review of Feasibility Study – Al Masane Project – For Arabian Shield Development Company and National Mining Company, WGM, February 20, 1989;

|

|

-

|

Feasibility Study on the Al Masane Project for Arabian Shield Development Company, July 22, 1994; and

|

|

-

|

Al Masane project, Mine Capital and Operating Cost Update, 1st Quarter 1996, WGM, April 1, 1996.

|

In April 2005 we retained SNC Lavalin Engineers & Constructors Inc. to update the capital and operating cost estimates for the Al Masane Project based on the engineering design work previously performed by Davy and WGM. SNC Lavalin determined that the estimated capital cost for development of the underground mine, a 2000 TPD concentrator, site access road, site power distribution, water pipeline, administration, service and camp buildings, and a tailing storage facility would be approximately $115,800,000. SNC Lavalin also estimated the extra cost associated with construction of a gold recovery circuit using cyanide leach to be $6,750,000. SNC Lavalin further determined that the total estimated operating cost for the project including a gold recovery circuit was $60.01 per ton with a level of accuracy of ± 15 percent.

In 2008 we retained Molinari & Associates Inc. to prepare cash flows and internal rate of return projections. Molinari used ore reserve estimates prepared by WGM in the July 22, 1994 Feasibility Study referenced above. Molinari developed a base case and four additional cash flow projections using the following assumptions:

|

-

|

Base Case: Production of 700,000 tpa for 11 years; capital investment increased to $139.5 million to allow for current tight machinery supply; and average metal 2007 YTD metal prices.

|

|

-

|

Scenarios 1-4: Production was increased to 840,000 tonnes during year 5 and further to 1,000,000 tonnes during year 9.

|

Messrs. H. Roger Schwall and Chris White

May 19, 2010

Page 10 of 17

Using discount rates of 5, 10 and 15 percent, Molinari determined Net Present Values of the project ranging from $258 million to more than $1 billion. A partial copy of the SNC Lavalin August 2005 Update of Feasibility Study and Molinari Cash Flow Projections are provided in Attachment D.

During this time in 2008, we believed that while the discount rates used by Molinari were on the low side, the overall profitability of the mining project was positive, even with metal prices at very low levels due to the economic situation in the world at the time. All of these factors were taken into account when the impairment analysis was performed.

Your comment made reference to ASC 360.10.35-21(f) SFAS 144, paragraph 8(f), which refers to assets which are disposed of or are likely to be disposed of. However, the Company noted, and notes, that paragraph 27 of SFAS 144 provides that “A long-lived asset to be disposed of other than by sale (for example, by abandonment, in an exchange measured based on the recorded amount of the nonmonetary asset relinquished, or in a distribution to owners in a spinoff) shall continue to be classified as held and used until it is disposed of. Paragraphs 7–26 shall apply while the asset is classified as held and used.” Since the assets were to be “disposed of” in the formation of the AMAK joint venture, which was to be “an exchange measured based on the recorded amount of the nonmonetary asset relinquished,” we believed that this instruction of paragraph 27 applied, and we performed the impairment assessment using the method specified in paragraphs 10 through 24 of SFAS 144. The carrying amount of the Saudi Arabian mining assets was significantly below both (i) the undiscounted net cash flow estimates set forth in the Molinari estimates, and (ii) the value of the assets implied by the terms for the formation of AMAK; therefore we concluded that there was no impairment.

With reserve calculations remaining relatively consistent over time, and production costs remaining very near where they were in the previous studies, the only variable in the cash flow projections for the asset was the price of metals on the world market. The Company consistently had Molinari review projected cash flow based upon changing metal prices and any other changes in costs or reserves which we became aware of over time. The negotiation with the joint venture partners was based upon this basic information, and the fact that the Company simply did not have the financial resources to develop this asset to the point of operation without such partners’ contributions of cash, local knowledge and expertise. Our discussions with consultants in the mining industry suggest that a mining project would likely be profitable for 5-7 years out of any 10 year period. This was proven correct in the decade of 2000 to 2010 as world metal prices sunk to low points in the 2000-2002 era and again for a short period in 2008. This being the case, the likelihood of negative cash flows for the project was considered to be in the 30-40 percent range. During negotiations with the partners, we believed that with sufficient capital, the likelihood of success was in the 60-70 percent range. The cash flow estimates and worksheet showing estimated costs, including interest costs, have been displayed on our web site continuously since early 2008.

As discussed in our response to comment 9 below, we believe that it is proper to continue to account for our investment in AMAK on the cost method. This will confirm to you that we have, and will continue to, evaluate the investment for impairment on a regular basis in accordance with the guidance in ASC 353-20-35-2 (APB No. 18, paragraph 6(a)), and that we will also consider the guidance in ASC 970.323.35-12 (SOP 78-9, paragraph 20).

Messrs. H. Roger Schwall and Chris White

May 19, 2010

Page 11 of 17

|

9.

|

We note your responses to prior comments 10 and 11 in our letter dated February 23, 2010. Please provide to us a more detailed analysis of how you applied the provisions of ASC 323.10.05 and ASC 323.10.15 (APB 18, paragraphs 16 and 17) when you determined that you should not record your share of AMAK’s losses for the period of December 31, 2008 through August 2009, and that you should discontinue using the

|

equity method of accounting beginning in August 2009. We note that your 41% interest results in a presumption that you have the ability to exercise significant influence over AMAK. In this regard, please discuss with greater detail how you considered the guidance provided at ASC 323.10.15 (FIN 35); including the examples presented in paragraph ASC 323.10.15-10 (FIN 35, paragraph 4). Tell us the efforts you have made to obtain financial information from AMAK and what access you have or could obtain to AMAK’s books and records as a result of your 41% ownership and four members on AMAK’s Board of Directors.

We note that if access is available to you and equity method accounting is appropriate, you would be expected to have audited financial statements prepared for AMAK’s operations in accordance with US GAAP upon which to base your equity method accounting, whether for the period from formation of AMAK through August 2009 or for all periods, even if this requires doing so at your own cost. Equity method accounting would also necessitate disclosures in accordance with Regulation S-X, Rules 3-09 and 4-08(g). Please provide support for your assertion that AMAK meets the definition of a foreign business.

We also note that if cost method accounting was appropriately applied, it would be inappropriate to include mineral reserve and related disclosures regarding AMAK’s assets and operations in your Form 10-K, given your lack of significant influence over those assets and operations. In addition, if cost method accounting was appropriately applied, disclosures should be provided addressing why the company is not able to exert significant influence over AMAK’s operations and how, and the expected period over which, the company will be able to recover its investment.

Response:

AMAK’s Classification as a Foreign Business. As we explained to you during our May 10, 2010 conference call, we believe that AMAK meets the definition of a foreign business under Section 6110.3 of the Division of Corporation Finance Financial Reporting Manual for the following reasons:

|

|

-

|

all of AMAK’s assets and operations are in Saudi Arabia

|

|

|

-

|

as set forth below, at all times at least 50%, and now more than 50%, of the common stock of AMAK was held by foreign businesses or individuals

|

Messrs. H. Roger Schwall and Chris White

May 19, 2010

Page 12 of 17

|

Stockholder

|

Original ownership

|

Ownership since August 2009

|

Nature and location of stockholder

|

|

Arabian American Development Company

|

50%

|

41%

|

U.S. corporation

|

|

Mr. Mohammed Aballala(a)

|

16%

|

18.88%

|

Saudi citizen

|

|

Thamarat Najran Co. Ltd. (a)

|

4%

|

4.72%

|

Saudi corporation

|

|

Al-Sha’er Trading, manufacturing and Contracting Company

|

10%

|

11.80%

|

Saudi corporation

|

|

His Royal Highness Prince Nawaf Bin Mishel Bin Saud Al Saud

|

8%

|

9.44%

|

Saudi citizen and member of the Saudi royal family

|

|

Mr. Ibraheem Bin Ali Bin Hussain Musallam (b)

|

5%

|

5.90%

|

Saudi citizen

|

|

Mr. Majed Bin Ali Bin Hussain Musallam (b)

|

5%

|

5.90%

|

Saudi citizen

|

|

Mr. Amer Bin Ali Bin Amer Babtain

|

2%

|

2.36%

|

Saudi citizen

|

(a) Mr. Mohammed Aballala is the majority stockholder of Thamarat Najran Co. Ltd.

(b) Mr. Ibrahim Bin Ali Bin Hussain Musallam and Mr. Majed Bin Ali Bin Hussain Musallam are brothers.

|

|

-

|

as set forth below, the majority of the members of AMAK’s board of directors are not resident in, or citizens of, the United States

|

|

Name of director

|

Citizenship and residence

|

|

Directors appointed by Arabian American Development Company

|

|

|

Nicholas Carter

|

United States

|

|

Ghazi Sultan

|

Saudi Arabia

|

|

Robert Kennedy

|

United States

|

|

Allen McKee

|

United States

|

|

Directors appointed by Saudi investors

|

|

|

Dr. Talal Al Shair (a)

|

Saudi Arabia

|

|

Ibrahim Musallam

|

Saudi Arabia

|

|

Mohammed Aballala

|

Saudi Arabia

|

|

Ayman Al-Shibl

|

Saudi Arabia

|

(a) Dr. Shair is the chairman of the board of AMAK, and under AMAK’s by-laws casts a ninth, tie breaking vote in cases where the vote of the eight directors is tied.

Status of August 2009 Amendments to AMAK Documents

As we discussed with you on the phone on May 19, 2010, we want to be sure that you understand the status, under Saudi law, of the amendments to AMAK’s Articles of Association and by-laws that were agreed to among the stockholders in August 2009.

Although all of the amendments were agreed to by all of the stockholders of AMAK, under Saudi law the amendments will not become official until adopted until they are approved by the Ministry of Commerce of Saudi Arabia. That approval process requires that (i) the amendments be approved by AMAK’s stockholders at a special (extraordinary) stockholders’ meeting attended by representatives of the Ministry of Commerce, (ii) AMAK publishes a notice of the amendments which allows stockholders to file formal objections to the proposed amendments, and (iii) the Ministry of Commerce then review and approve the amendments, including the

Messrs. H. Roger Schwall and Chris White

May 19, 2010

Page 13 of 17

consideration of any objections raised by AMAK stockholders. AMAK has scheduled a stockholders’ meeting for June 2010 at which the approval of the amendments will be voted upon. Although these official requirements for the adoption of the amendments have not yet been completed, the Company believes that the amendments will be approved, and the Company and the Saudi investors have since August 2009 been conducting the affairs of AMAK pursuant to the proposed amendments.

In particular, we believe that it is highly unlikely that the Saudi authorities would object to amendments to AMAK’s governing documents in light of the facts that (i) all of the stockholders agreed to the amendments in August 2009, and thus will vote to approve the amendments at the required extraordinary meeting, and (ii) the amendments increase (rather than decrease) the ownership of the Saudi investors, and limit the period during which the foreign investor (our company), rather than the Saudi investors, has the right to appoint directors.

We intend to expand Note 8, as illustrated in Attachment F, to more fully describe the status of the amendments.

Application of Equity Accounting From December 31, 2008 to August 2009

As we explained to the staff in our phone call on May 10th, in applying the equity method of accounting for the period from December 31, 2008, until August 2009, at the time the Company prepared its 2009 financial statements (March 2010) the Company made its best estimate of AMAK’s net income or loss for that period, stated under U.S. generally accepted accounting principles (“U.S. GAAP”). In making that estimate, the Company relied on its knowledge of the activities and operations that had taken place at AMAK for the period December 31, 2008, to August 2009.

As disclosed in Note 8 to our 2009 financial statements, during the period from December 2008 until August 2009 we were aware that AMAK’s activities “during that period were the construction of facilities to begin the commercial development of the interests.” Accordingly, we concluded that virtually all of AMAK’s expenditures during that period were likely to be of the type capitalizable under U.S. GAAP and that our share of AMAK’s net income or loss for that period would be immaterial.

In May 2010 we received a draft of AMAK’s 2009 and 2008 financial statements prepared under generally accepted accounting principles in Saudi Arabia (“Saudi GAAP”) and stated in Saudi Riyals (“SR”). The financial statements were being audited by Deloitte & Touche Saudi Arabia under generally accepted auditing standards in Saudi Arabia (“Saudi GAAS”). Those draft financial statements indicate the following:

|

|

-

|

during the year ended December 31, 2009, there were under Saudi GAAP no items of income or expense. The draft financial statements state that “The Company has not yet commenced its commercial operations. The Company is not reporting a statement of income as no material expenses of a revenue nature were incurred during the period.”

|

|

|

-

|

for the year ended December 31, 2008, the only item of income or expense was an accrual for Zakat taxes of SR 1,965,000 (approximately $525,000). (We discuss below how we intend to account for our 50% share of this expense.) The Zakat tax is an “alms tax” (a tithe tax) levied upon Saudi corporations and individuals “of sufficient means.” The tax is not calculated on income, but rather is based on “wealth” as defined in the statutes with wealth derived from different types of assets taxed at different rates, and its

|

Messrs. H. Roger Schwall and Chris White

May 19, 2010

Page 14 of 17

| |

-

|

assessment derives from the Islamic laws requiring those of sufficient means to tithe. There was no Zakat tax for 2009 as AMAK’s “wealth,” as defined, was negative. Additionally, the Zakat tax is only assessed on the “wealth” attributable to the portion of a corporation owned by Saudi shareholders.

|

The draft financial statements indicate that during 2009 AMAK capitalized expenditures of approximately SR 116 million (approximately $30,972,000) as additions to property and equipment. The accounting policy stated in the draft financial statements is as follows:

“Pre-operating expenses consist of the incorporation costs incurred in setting up the Company and exploration costs. Incorporation costs are amortized using the straight line method over a period of 7 years. Exploration costs are expensed in the period incurred until a mine is identified as having economical development potential. Pre-operating costs incurred on mines that have economical development potential are deferred net of proceeds from the sale of any production during the development period and then amortized over the shorter of the expected life of the mine or a period of seven years. If a mine is no longer considered economical, the accumulated project costs are charged to the statement of income in the year in which the determination is made.”

With the exception of the accounting for the incorporation costs, we believe that the accounting policy stated above is similar to accounting that would be acceptable under U.S. GAAP. The organizational costs for AMAK, which would have to be expensed under U.S. GAAP, were mostly those incurred and contributed by our Company, and as we disclosed in Note 2 to our 2009 financial statements, we restated our 2008 financial statements to record in that year our 50% of those organizational costs.

You asked us to discuss the possibility that there were some costs of an administrative nature at AMAK that could not be capitalized under U.S. GAAP. To our knowledge, all of the employees at AMAK, except for a bookkeeper, have been directly involved in the development of the mine, and thus their salaries would be capitalized. In addition, we are not aware of any material expenditures for outside services in 2009 that did not relate to the mine development. With respect to AMAK’s accounting function, as we indicated to you in our prior letter, in 2009 AMAK’s accounting function consisted of one bookkeeper who functioned as a bill payer and check writer. While the costs associated with this function should be expensed under U.S. GAAP, we do not believe the costs for this one individual would be material.

Accordingly, we believe that we had a reasonable basis in March 2010 for our estimate that for the period December 31, 2008, to August 2009 our share of AMAK’s net income or loss would not be material, and we believe the additional information that has become available to us subsequent to the issuance of our 2009 financial statements supports our conclusion.

As discussed above, when we received the draft 2009 financial statements, we first learned that there had been a 2008 accrual for Zakat taxes of $525,000. We intend to record a charge for our 50% share of this ($262,500) in the second quarter of 2010 on the basis that our receipt of this information in that period (which information was not available when the 2008 financial statements were issued) causes us to revise our original estimate of our share of AMAK’s 2008 net income or loss. The notes to the financial statements for that Form 10-Q will include appropriate disclosures regarding the nature and effect of the revision of this estimate.

Messrs. H. Roger Schwall and Chris White

May 19, 2010

Page 15 of 17

August 2009 Change to the Cost Method of Accounting

As we discussed with you, we believe that our change in August 2009 from the equity method of accounting to the cost method of accounting is supported by both FIN 35, paragraph 4(d) and FIN 35, paragraph 4(c).

FIN 35, paragraph 4(d). Under paragraph 4(d) of FIN 35, the presumption that a holder of more than a 20% voting interest has significant influence is overcome if “The investor needs or wants more financial information to apply the equity method than is available to the investee's other shareholders (for example, the investor wants quarterly financial information from an investee that publicly reports only annually), tries to obtain that information, and fails.”

In addition, paragraph 4 of FIN 35 indicates that “It may be necessary to evaluate the facts and circumstances for a period of time before reaching a judgment.”

We explained to you that the by-laws (both the original by-laws and the by-laws as amended) of AMAK:

|

|

-

|

provide that the auditor shall audit the financial statements of AMAK and shall present the financial statements to AMAK’s annual meeting (Article 45); and

|

|

|

-

|

provide that the annual meeting shall be held within the first six months of the year (Article 33).

|

Thus, effectively the by-laws require that the audited financial statements for each December 31 fiscal year prepared under Saudi GAAP and audited under Saudi GAAS, be issued on or before June 30 of the following year.

The by-laws of AMAK do not provide our Company, either through our representatives on AMAK’s board, or as a stockholder of AMAK, the right to access the accounting or other financial records of AMAK.

As we explained, prior to this time our efforts and requests to have AMAK produce the financial statements (i.e., unaudited quarterly and audited annual financial statements prepared under U.S. GAAP and audited under U.S. GAAS) that we would need to apply the equity method of accounting have been informal and have not been responded to.

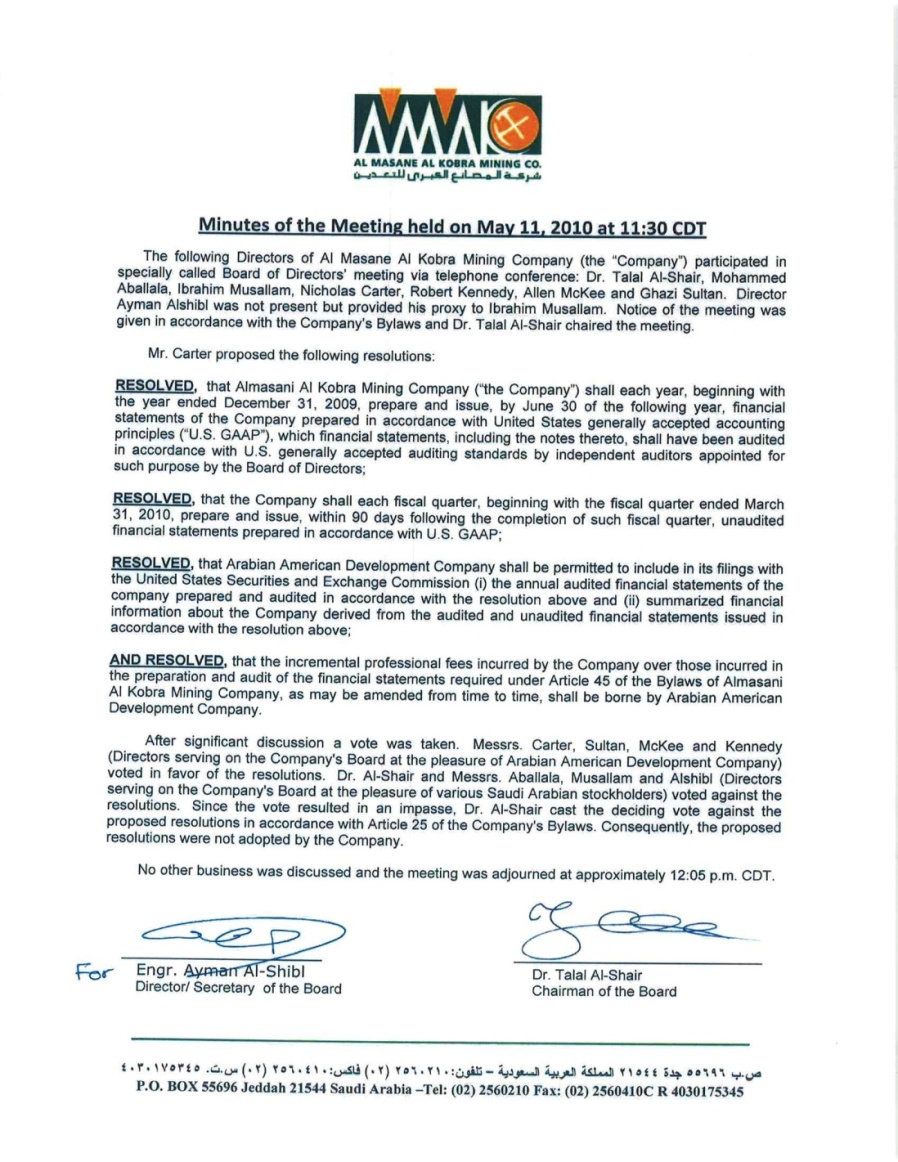

However, on May 11, 2010, our members of AMAK’s board of directors called for a meeting of the AMAK board, and at that meeting put forward the following resolutions:

RESOLVED, that Almasani Al Kobra Mining Company (“the Company”) shall each year, beginning with the year ended December 31, 2009, prepare and issue, by June 30 of the following year, financial statements of the Company prepared in accordance with United States generally accepted accounting principles (“U.S. GAAP”), which financial statements, including the notes thereto, shall have been audited in accordance with U.S. generally accepted auditing standards by independent auditors appointed for such purpose by the Board of Directors;

RESOLVED, that the Company shall each fiscal quarter, beginning with the fiscal quarter ended March 31, 2010, prepare and issue, within 90 days following

Messrs. H. Roger Schwall and Chris White

May 19, 2010

Page 16 of 17

the completion of such fiscal quarter, unaudited financial statements prepared in accordance with U.S. GAAP;

RESOLVED, that Arabian American Development Company shall be permitted to include in its filings with the United States Securities and Exchange Commission (i) the annual audited financial statements of the Company prepared and audited in accordance with the resolution above and (ii) summarized financial information about the Company derived from the audited and unaudited financial statements issued in accordance with the resolution above;

AND RESOLVED, that the incremental professional fees incurred by the Company over those incurred in the preparation and audit of the financial statements required under Article 45 of the Bylaws of Almasani Al Kobra Mining Company, as may be amended from time to time, shall be borne by Arabian American Development Company.

The four directors appointed by us voted in favor of these resolutions while the four directors appointed by the Saudi stockholders voted against the resolutions. Under AMAK’s by-laws, a ninth tie breaking vote was then granted to the chairman of the AMAK directors, Dr. Talal Al Shair, who voted against the resolutions. The resolutions were thus defeated. A copy of the minutes of this meeting, signed by the Chairman and Secretary of the Board of AMAK, are attached as Attachment E.

FIN 35, paragraph 4(c). Paragraph 4(c) of FIN 35 provides that the presumption that a holder of more than a 20% voting interest has significant influence would be overcome if “Majority ownership of the investee is concentrated among a small group of shareholders who operate the investee without regard to the views of the investor.”

As we explained to you on May 10th, we believe that these circumstances exist. Due to the unique business, regulatory and cultural environments in Saudi Arabia, we have found that we are totally dependent on the efforts of the Saudi investors to move the development of the mining project forward through regulatory and financing processes. As a result, we have found that it is unwise to openly disagree with the Saudi investors when they have expressed a unified view as to a course of action.

We describe to you the following examples of this:

|

|

-

|

when the AMAK Board selected an auditor, we believed that either Moore Stephens, because it was the Travis Wolff affiliate, or KPMG, because of its experience auditing mining operations, would be the best choices. Notwithstanding, the Saudi directors selected Deloitte due to prior experience with that firm without even a formal vote on the Moore Stephens or KPMG firms.

|

|

|

-

|

AMAK had contracted with a Chinese firm for the construction of certain underground facilities preparatory to the production of ore. While that firm was selected, the Saudi directors believed that it should work under the direction of a Saudi general contractor, and took that course of action notwithstanding our stated position that the Chinese firm was well qualified to do the work and did not need a supervising general contractor.

|

We noted to you that we had found another company which cited such factors in supporting its use of the cost accounting method where it held a voting interest in excess of 20%. Specifically, Celanese Corporation states on page 92 of its 2009 Form 10-K that:

Messrs. H. Roger Schwall and Chris White

May 19, 2010

Page 17 of 17

“Certain investments where the Company owns greater than a 20% ownership interest are accounted for under the cost method of accounting because the Company cannot exercise significant influence over these entities. The Company determined that it cannot exercise significant influence over these entities due to local government investment in and influence over these entities, limitations on the Company’s involvement in the day-to-day operations and the present inability of the entities to provide timely financial information prepared in accordance with US GAAP.”

As the result of the facts and circumstances described above, we believe that it was proper to change from the equity method to the cost method to account for our investment in AMAK in August 2009.

Conclusion regarding the use of the cost method. As a result of the above, we believe that the conditions of paragraph 4(d) of FIN 35 are present. We also believe, as we discussed with you, that the condition of paragraph 4(d) of FIN 35 is generally determinative that equity method accounting cannot be applied, and you did not object to that position.

Changes to Item 1 – Business

In accordance with your request, we have revisited the nature of the disclosures regarding AMAK contained in Part I, Item 1 of our 2009 Form 10-K and we are making appropriate revisions to reflect the fact that we lack any significant influence over the operations of AMAK and that we are dependent on the efforts of the Saudi investors for the success of the project.

Changes to Note 8 to the Financial Statements

In order to more clearly state the rational for our change to the cost method of accounting in August 2009 (based on the facts available to us the time our 2009 financial statements were originally issued and without reference to subsequent events), we plan to make small changes to Note 8 to our financial statements. A draft of those changes is attached as Attachment F.

The Company hereby acknowledges that it is responsible for the adequacy and accuracy of the disclosure in the filing; that SEC staff comments or changes to disclosure in response to staff comments do not foreclose the SEC from taking any action with respect to the filing; and the Company may not assert staff comments as a defense in any proceeding initiated by the SEC or any person under the federal securities laws of the United States.

Thank you for your consideration.

Sincerely,

/s/ Connie Cook

Connie Cook

Chief Accounting Officer

ATTACHMENT A

(Response to SEC Question No. 2)

Item 11. Executive Compensation

Report of the Compensation Committee

The Compensation Committee has reviewed and discussed with management the following Compensation Discussion and Analysis. Based on such review and discussion, the Compensation Committee has recommended to the Board of Directors that the following Compensation Discussion and Analysis be included in the Form 10-K for the year ended December 31, 2009.

Members of the Compensation Committee

Allen P. McKee, Chairman

Robert Kennedy

Ghazi Sultan

Mohammed Al-Omair

Compensation Discussion and Analysis

Introduction

This discussion presents the principles underlying our executive officer compensation program. Our goal in this discussion is to provide the reasons why we award compensation as we do and to place in perspective the data presented in the tables that follow this discussion. The focus is primarily on compensation of our executive officers for the fiscal year ended December 31, 2009, but some historical and forward-looking information is provided to put such year’s compensation information in context. The information presented herein relates to Nicholas N. Carter, our Chief Executive Officer since July 1, 2009, Connie Cook, our Chief Accounting Officer, Mark Williamson, our Vice-President of Marketing, and our two other most highly compensated employees, who are sometimes referred to in this Form 10-K as our “Executives.” For purposes of this discussion, we did not include Mr. El-Khalidi as an Executive due to his retirement from the Chief Executive Officer position on June 30, 2009.

It is the intent of the Board that the salaries and other compensation of the executives of the Company will be recommended to the Board for action at least once annually and will be based upon competitive salaries and financial performance of the Company. The Compensation Committee has overall responsibility for the approval, evaluation and oversight of all of the Company’s compensation plans. The Committee’s primary purpose is to assist the Company’s Board in the discharge of its fiduciary responsibilities relating to fair and competitive compensation. The Compensation Committee meets in the fourth quarter of each year to review the compensation program and to determine compensation levels for the ensuing fiscal year and at other times as required.

Objectives of the Compensation Programs

The compensation programs of the Company are designed to attract and retain qualified individuals upon whom the sustained progress, growth, profitability, and value of the Company depend. It is the plan of the Board that through the Compensation Committee, the Company will develop and implement compensation policies, plans and programs to further these goals by rewarding executives for positive financial performance. Management provides recommendations regarding executive compensation to the Compensation Committee. The Company’s executive compensation program is intended to align the interests of its management team with those of its shareholders by motivating the Executives to achieve strong financial and operating results for the Company, which it believes closely correlates to long–term shareholder value. In addition, the Company’s program is designed to achieve the following objectives:

|

|

• attract and retain talented Executives by providing reasonable total compensation levels competitive with that of executives holding comparable positions in similarly situated organizations;

|

• provide total compensation that is justified by individual performance;

|

|

• provide performance–based compensation that balances rewards for short–term and long–term results and is tied to both individual and the Company’s performance; and

|

|

|

• encourage the long–term commitment of our Executives to the Company and its shareholders’ long–term interests.

|

What the Compensation Programs are Designed to Reward

The compensation programs are designed to reward performance that contributes to the achievement of the Company’s business strategy on both a short–term and long–term basis. In addition, the Company rewards qualities that it believes help achieve its strategy such as teamwork; individual performance in light of general economic and industry specific conditions; performance that supports the Company’s core values; resourcefulness; the ability to manage existing assets; the ability to explore new avenues to increase profits, level of job responsibility; and tenure. The Company does not currently engage any consultant related to executive and/or director compensation matters, although the Company is currently soliciting proposals from various compensation consultants located in the Houston, Texas area for assistance in 2010 and future years.

Elements of the Company’s Compensation Program and Why It Pays Each Element

To accomplish its objectives, the Company seeks to offer a total direct compensation program to its Executives that, when valued in its entirety, serves to attract, motivate and retain executives with the character, experience and professional accomplishments required for the Company’s growth and development. The Company’s compensation program is comprised of four elements:

• base salary;

• incentive compensation;

• stock option plan; and

• benefits.

Base Salary.

We pay our Executives a base salary, which we review and determine annually. We believe that a competitive base salary is a necessary element of any compensation program. We believe that attractive base salaries can motivate and reward the Executives for their overall performance. Base salaries are established in part based on the particular executive’s position, responsibility, experience, skills and expected contributions during the coming year and such individual’s performance during the prior year. We also have sought to align base compensation levels comparable to our competitors and other companies of similar size. We do not view base salaries as primarily serving our objective of paying for performance, but in attracting and retaining the most qualified executives necessary to run the Company’s business. The base salaries of our Executives have been subject to a standard cost of living increase annually over the past several years at the same rate as other Petrochemical Segment employees. In 2009, we gave all employees of the Company, including the Executives, a 4 percent cost of living adjustment. In addition, Mr. Carter’s annual salary was increased to $250,000 effective July 1, 2009, due to his promotion to Chief Executive Officer.

Cash Incentive Bonuses.

The primary objective of our annual cash incentive bonus program is to motivate and reward our Executives for meeting our short-term objectives using a pay-for-performance program with objectively determinable performance goals. Executives are eligible to receive a cash incentive bonus under the 2009 Executive Cash Bonus Plan (“CBP”), which was recommended and adopted by the Compensation Committee. The objectives of the CBP are to align the interests of the Executives with the Company’s annual performance goals. The CBP focuses on rewarding executives for the achievement of annual financial objectives with competitive financial incentives, and provides a systemic plan for establishing definitive performance goals. The Company’s performance goals are based on growth in income before tax expense (“IBT”). Executives will be awarded cash bonus compensation based on the Company’s annual results in this area. Target awards and weightings may be modified by the Compensation Committee during the plan year based upon a shift in focus or changing industry standards, or any other factors that the Compensation Committee deems appropriate. The Compensation Committee has the authority to administer the CBP and has the final decision on any discrepancies in interpretation of the CBP.

The amount of money, if any, in the CBP will be calculated based on the overall level of achievement with respect to IBT. Any awards are paid after completion of the Company’s audited financial statements for the applicable year. Participants will not be entitled to receive an award unless they are employed by the Company at the end of the applicable plan year and at the time the award is paid by the Company.

The performance objective for earning an award under the CBP relates to the Company’s IBT. The Company’s IBT is required to exceed $10 million (the “Threshold Amount”) in order for funds to be allocated to the CBP. The amount allocated to the CBP is approximately 1.0 percent of IBT which is based primarily on historical levels of cash bonuses given to Executives since 2005 (the “base year”). The Compensation Committee then typically allocates approximately 40-50 percent of the CBP, if any, as a cash bonus award to the Chief Executive Officer. The Chief Executive Officer then submits recommendations to the Compensation Committee regarding division of the remainder of the CBP between the other Executives as cash bonus awards.

For the fiscal year ended December 31, 2009, the amount allocated to the CBP was $130,000, which was paid to our Executives as cash bonuses in the first quarter of calendar year 2010.

Equity Compensation.

We believe that stock options are an important long-term incentive for our Executives and that our stock option program has been effective in aligning executive interests with those of our stockholders. We review our equity compensation plans annually. The Executives are eligible for annual stock option grants based on targeted levels. These options are intended to produce value for each Executive if (i) our stockholders derive significant sustained value and (ii) the Executive remains employed with us.

In 2009 the Company did not have any program, plan or obligation under which it was required to grant equity compensation to any Executive on specified dates or upon the achievement of certain performance goals. The Company’s 2008 Stock Option Plan for Key Employees governs discretionary stock option grants to Executives. The authority to make equity grants to Executives rests with the Compensation Committee, although, as noted, the Compensation Committee does consider the recommendations of our Chief Executive Officer in setting the compensation of our other Executives. No stock option grants were awarded during the year ended December 31, 2009. Stock options were awarded during the first quarter of 2010 based on 2009 results and the results of an informal peer group analysis conducted by the Compensation Committee. Stock option awards vest over time, whereby, in each case, 100% percent of the award will vest two years from the date of grant and the options expire seven years from the date of grant.

As noted previously, on June 30, 2009, Mr. El-Khalidi retired as Chief Executive Officer of the Company. On July 2, 2009, the Board of Directors considered Mr. El-Khalidi’s efforts related to the Al Masane mining project in southwestern Saudi Arabia in conjunction with his retirement. The Board determined

that the Company should issue two options to purchase a total of 400,000 shares to Mr. El-Khalidi, tied to the performance of AMAK. The rationale for the grant of these two options was based on the fact that virtually all of Mr. El-Khalidi’s career was spent working on the mining project in Saudi Arabia under difficult conditions and the Board believed a substantial award was justified in light of his relatively low salary of $72,000 per annum. To achieve a linkage of the value of the award to the ultimate success of the Saudi Arabian mining project, the Board of Directors made the options contingent upon the occurrence of the following conditions which are explicitly tied to the performance of AMAK: (i) the first option for 200,000 shares cannot be exercised until such time as the first shipment of ore from the mining project is transported for commercial sale by AMAK and the option terminates if not exercised by June 30, 2012, and (ii) the second option for 200,000 shares cannot be exercised until such time as the Company receives its first cash dividend distribution from AMAK and the option terminates if not exercised by June 30, 2019.

Perquisites.

The Company provides benefits to all employees that it believes are standard in the industry. These benefits consist of a group medical and dental insurance program for employees and their qualified dependents, group life insurance for employees and their spouses, accidental death and dismemberment coverage for employees, a Company sponsored cafeteria plan and a 401(k) employee savings and investment plan. The Company matches employee deferral amounts, including amounts deferred by named executive officers, up to a total of 6% of the employee’s eligible salary, excluding annual cash bonuses, subject to certain regulatory limitations. Our use of perquisites as an element of compensation is very limited. We do not view perquisites as a significant element of our comprehensive compensation structure.

The Compensation Committee Process

Compensation Committee meetings typically involve a preliminary discussion with our Chief Executive Officer prior to the Compensation Committee deliberating without any members of management present. For compensation decisions, including decisions regarding the grant of stock options relating to executive officers (other than our Chief Executive Officer); the Compensation Committee considers the recommendations of our Chief Executive Officer and includes him in its discussions.

Peer Group

As noted, the Compensation Committee utilized a small peer group of similarly sized companies as a reference for determining competitive total compensation packages for our Executives. For 2009 compensation, this peer group consisted of the following companies:

Crosstex

Global Partners

Rentech

KMG Chemical

Syntroleum

Penford Corp

Adams Resources & Energy Inc.

Synthesis Energy

American Pacific Corporation

Sulphco Inc.

Sterling Chemicals Inc.

Regulatory Considerations

We account for the equity compensation expense for our employees under the rules of Financial Accounting Standards Board (FASB) Accounting Standards Codification (ASC) Topic 718 (“ASC 718”), which requires us to estimate and record an expense for each award of equity compensation over the service period of the award. Accounting rules also require us to record cash compensation as an expense at the time the obligation is accrued.

Employment Arrangements

The Company has not entered into definitive employment agreements with any of its executive officers. All executive officers serve at the discretion of the Board with no fixed term of employment.

Cash and Other Compensation

South Hampton’s profit sharing program is available to all employees based upon South Hampton’s quarterly performance. Since South Hampton is located about an hour north of a larger petrochemical sector, competition for qualified, intelligent, conscientious employees is high. Base pay for employees is typically about 20% less than larger facilities; however, the profit sharing program allows South Hampton to compensate employees with additional pay when profits are sound. It also enables South Hampton the ability to forego payments during times of economic slowdown. There is no set formula for calculating profit sharing as it is based upon several factors including profit, cash flow, expectations and special cash needs of South Hampton and the Company.

The following table, which should be read in conjunction with the explanations provided above, sets forth summary compensation information for the year ended December 31, 2009 for the Company’s (i) Chief Executive Officer, (ii) Chief Accounting Officer, and (iii) each of the Company’s three most highly compensated executives other than the Chief Executive Officer and the Chief Accounting Officer who were serving as executive officers of the Company as of December 31, 2009.

2009 Summary Compensation Table

|

Name and

Principal Position

|

Year

|

|

Salary

($)

|

|

|

Bonus

($)(1)

|

|

|

Profit Sharing

($)

|

|

|

Restricted

Stock

Award(s)

($)

|

|

|

Option Award(s)

($)(2)

|

|

|

All Other

Compensation

($) (3)(4)(5)

|

|

|

Total ($)

|

|

|

Hatem El Khalidi

President and Chief

Executive Officer until June 30, 2009, Director

|

2009

|

|

$ |

36,000 |

|

|

$ |

31,500 |

|

|

|

-- |

|

|

|

-- |

|

|

$ |

186,288 |

|

|

$ |

40,000 |

|

|

$ |

293,788 |

|

|

2008

|

|

$ |

72,000 |

|

|

|

-- |

|

|

|

-- |

|

|

|

-- |

|

|

|

-- |

|

|

$ |

8,000 |

|

|

$ |

80,000 |

|

|

2007

|

|

$ |

72,000 |

|

|

|

-- |

|

|

|

-- |

|

|

|

-- |

|

|

|

-- |

|

|

$ |

8,000 |

|

|

$ |

80,000 |

|

|

Nicholas N. Carter President and Chief

Executive Officer since July 1, 2009; previously

Executive Vice President and Chief Operating Officer

|

2009

|

|

$ |

234,837 |

|

|

$ |

60,000 |

|

|

$ |

42,552 |

|

|

|

-- |

|

|

|

-- |

|

|

$ |

14,090 |

|

|

$ |

351,479 |

|

|

2008

|

|

$ |

209,918 |

|

|

|

-- |

|

|

$ |

28,665 |

|

|

$ |

99,800 |

|

|

|

-- |

|

|

$ |

12,595 |

|

|

$ |

350,978 |

|

|

2007

|

|

$ |

172,059 |

|

|

$ |

50,000 |

|

|

$ |

46,506 |

|

|

$ |

66,000 |

|

|

|

-- |

|

|

$ |

10,324 |

|

|

$ |

344,889 |

|

|

Connie J. Cook

Chief Accounting Officer

|

2009

|

|

$ |

142,208 |

|

|

$ |

30,000 |

|

|

$ |

32,715 |

|

|

|

-- |

|

|

|

-- |

|

|

$ |

8,533 |

|

|

$ |

213,456 |

|

|

2008

|

|

$ |

133,009 |

|

|

|

-- |

|

|

$ |

26,143 |

|

|

$ |

49,900 |

|

|

|

-- |

|

|

$ |

7,981 |

|

|

$ |

217,033 |

|

|

2007

|

|

$ |

108,500 |

|

|

$ |

25,000 |

|

|

$ |

45,085 |

|

|

$ |

33,000 |

|

|

|

-- |

|

|

$ |

6,510 |

|

|

$ |

218,095 |

|

|

Mark D. Williamson

Vice President of Marketing, Petrochemical Company

|

2009

|

|

$ |

227,500 |

|

|

$ |

40,000 |

|

|

$ |

32,652 |

|

|

|

-- |

|

|

|

-- |

|

|

$ |

13,650 |

|

|

$ |

313,802 |

|

|

2008

|

|

$ |

240,705 |

|

|

|

-- |

|

|

$ |

26,143 |

|

|

$ |

49,900 |

|

|

|

-- |

|

|

$ |

14,442 |

|

|

$ |

331,190 |

|

|

2007

|

|

$ |

190,393 |

|

|

$ |

25,000 |

|

|

$ |

45,023 |

|

|

|

-- |

|

|

|

-- |

|

|

$ |

11,424 |

|

|

$ |

271,840 |

|

|

Gerardo Maldonado,

Account Representative,

Petrochemical

Company

|

2009

|

|

$ |

192,543 |

|

|

|

-- |

|

|

$ |

24,437 |

|

|

|

-- |

|

|

|

-- |

|

|

$ |

11,553 |

|

|

$ |

228,533 |

|

|

2008

|

|

$ |

179,158 |

|

|

|